Generative models for the request for quote activity¶

Simulation of RfQs arrival and client attrition¶

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from scipy.stats import poisson, norm

from collections import deque

def run_simulation(N_clients=50,

T=200,

reservation_price_mean=100,

reservation_price_std_pct=0.1,

lambda_mean=1,

lambda_std=0.05,

prior_mean=60,

prior_std=10,

res_price_noise_std_pct=0.2,

hit_rate_target=0.4,

window_size=10,

attrition_threshold=0.1):

"""

Simulate RFQ interactions with Bayesian quantile pricing and client attrition.

Clients stop trading if their moving-average hit rate over `window_size` days falls below `attrition_threshold`.

Returns:

rfq_df: DataFrame of RfQ events

active_history: list of active client counts per day

activity_matrix: binary DataFrame of daily activity (clients x days)

"""

np.random.seed(42)

# Generate distribution of reservation prices for the segment of clients

reservation_prices = np.random.normal(reservation_price_mean,

reservation_price_mean * reservation_price_std_pct,

N_clients)

# Reservation prices are noisy given potential changing market conditions

res_price_noise_std = res_price_noise_std_pct * reservation_price_mean

res_price_noise_var = res_price_noise_std**2

# Generate distribution of RfQ intensities for the segment of clients

lambdas = np.abs(np.random.normal(lambda_mean, lambda_std, N_clients))

clients_posterior = {i: {'mean': prior_mean, 'var': prior_std**2,

'n': 0, 'sum_obs': 0.0}

for i in range(N_clients)}

z = norm.ppf(1 - hit_rate_target)

active = np.ones(N_clients, dtype=bool)

# Track per-client active status at end of each day

active_flags = np.zeros((T, N_clients), dtype=bool)

daily_history = [deque(maxlen=window_size) for _ in range(N_clients)]

active_history = []

records = []

Y = np.zeros((T, N_clients), dtype=int)

for t in range(T):

daily_hits = np.zeros(N_clients, dtype=int)

daily_reqs = np.zeros(N_clients, dtype=int)

for i in range(N_clients):

if not active[i]: continue

n_rfq = poisson.rvs(lambdas[i])

if n_rfq > 0: Y[t,i] = 1

for _ in range(n_rfq):

post = clients_posterior[i]

price = max(0.0, post['mean'] + np.sqrt(post['var'] + res_price_noise_var) * z)

r = norm.rvs(reservation_prices[i], res_price_noise_std)

# Trading happens when price offered is lower than the reservation price

hit = price <= r

daily_reqs[i] += 1; daily_hits[i] += int(hit)

# The dealer updates the estimation of the reservation price of the client

post['n'] += 1; post['sum_obs'] += r

post_var = 1/(1/prior_std**2 + post['n']/res_price_noise_var)

post['var'] = post_var

post['mean'] = post_var*(prior_mean/prior_std**2 + post['sum_obs']/res_price_noise_var)

records.append({'time': t, 'client_id': i, 'price': price, 'hit': hit})

for i in range(N_clients):

if not active[i] or daily_reqs[i]==0: continue

rate = daily_hits[i]/daily_reqs[i]

daily_history[i].append(rate)

# A client stops sending RfQs to the dealer if the hit & miss is too low

if len(daily_history[i])==window_size and np.mean(daily_history[i])<attrition_threshold:

active[i] = False

active_history.append(active.sum())

active_flags[t, :] = active.copy()

rfq_df = pd.DataFrame(records)

activity = pd.DataFrame(Y, columns=[f'client_{i}' for i in range(N_clients)])

active_df = pd.DataFrame(active_flags, columns=[f'client_{i}' for i in range(N_clients)])

return rfq_df, active_history, activity, active_df

from scipy.special import betaln

from scipy.optimize import minimize

# ----------------------

# Segment-level Model

# ----------------------

def estimate_segment_params(activity_matrix):

def log_marginal_likelihood(D, alpha, beta, gamma, delta):

n, x = len(D), D.sum()

last = np.where(D==1)[0]

r = n - (last[-1]+1) if last.size>0 else n

logA = (betaln(alpha+x, beta+n-x)-betaln(alpha,beta)

+betaln(gamma, delta+n)-betaln(gamma,delta))

logB = [(betaln(alpha+x, beta+n-x-i)-betaln(alpha,beta)

+betaln(gamma+1, delta+n-i)-betaln(gamma,delta))

for i in range(1, r+1)]

mags = [logA] + logB; m_max = max(mags)

return m_max + np.log(sum(np.exp(m - m_max) for m in mags))

def neg_ll(params):

alpha, beta, gamma, delta = np.exp(params)

return -sum(log_marginal_likelihood(activity_matrix.iloc[:end, j].values,

alpha, beta, gamma, delta)

for j in range(activity_matrix.shape[1])

for end in [activity_matrix.iloc[:,:].values.shape[0]])

res = minimize(neg_ll, np.log([1,1,1,1]), method='L-BFGS-B', bounds=[(-5,5)]*4)

return np.exp(res.x)

def attrition_probability(D, alpha, beta, gamma, delta):

n, x = len(D), D.sum()

last = np.where(D==1)[0]

r = n - (last[-1]+1) if last.size>0 else n

logA = (betaln(alpha+x, beta+n-x)-betaln(alpha,beta)

+betaln(gamma, delta+n)-betaln(gamma,delta))

logB = [(betaln(alpha+x, beta+n-x-i)-betaln(alpha,beta)

+betaln(gamma+1, delta+n-i)-betaln(gamma,delta))

for i in range(1, r+1)]

mags = [logA] + logB; m_max = max(mags)

logL = m_max + np.log(sum(np.exp(m - m_max) for m in mags))

P_active = np.exp(logA - logL)

return 1 - P_active

from sklearn.metrics import (

confusion_matrix, accuracy_score,

precision_score, recall_score,

roc_curve, auc

)

# ----------------------

# Workflow: Simulate, Train, Test

# ----------------------

T_train, T_test = 100, 100

T_tot = T_train + T_test

N_clients = 50

rfq_all, active_all, Y_all, active_df = run_simulation(N_clients = N_clients, T=T_train+T_test)

Y_train = Y_all.iloc[:T_train].reset_index(drop=True)

Y_test = Y_all.iloc[T_train:].reset_index(drop=True)

rfq_test = rfq_all[rfq_all['time']>=T_train].copy()

rfq_test['time'] -= T_train

active_test = active_all[T_train:]

alpha, beta, gamma, delta = estimate_segment_params(Y_train)

print(f"Params: α={alpha:.2f}, β={beta:.2f}, γ={gamma:.2f}, δ={delta:.2f}")

# ----------------------

# Risk Scoring

# ----------------------

risk_records = []

for j in range(Y_test.shape[1]):

hist = []

for t in range(T_test):

hist.append(Y_test.iloc[t, j])

D = np.array(hist, dtype=int)

p_inact = attrition_probability(D, alpha, beta, gamma, delta)

risk_records.append({

'time': t,

'client_id': j,

'p_inactive': p_inact,

'alert': p_inact > 0.5 # thresholded prediction

})

risk_df = pd.DataFrame(risk_records)

# Label inactivity

risk_df['inactive'] = risk_df.apply(

lambda r: not active_df.loc[r['time'] + T_train, f'client_{r["client_id"]}'],

axis=1

)

# ----------------------

# Evaluation Metrics

# ----------------------

# Ground truth and predictions

y_true = risk_df['inactive']

y_pred = risk_df['alert'] # at 0.5 threshold

y_scores = risk_df['p_inactive'] # raw probabilities

# Confusion matrix

tn, fp, fn, tp = confusion_matrix(y_true, y_pred).ravel()

print("Confusion Matrix:")

print(f" TN={tn}, FP={fp}, FN={fn}, TP={tp}")

# Accuracy, Precision, Recall at 0.5

accuracy = accuracy_score(y_true, y_pred)

precision = precision_score(y_true, y_pred)

recall = recall_score(y_true, y_pred)

print(f"Accuracy : {accuracy:.4f}")

print(f"Precision: {precision:.4f}")

print(f"Recall : {recall:.4f}")

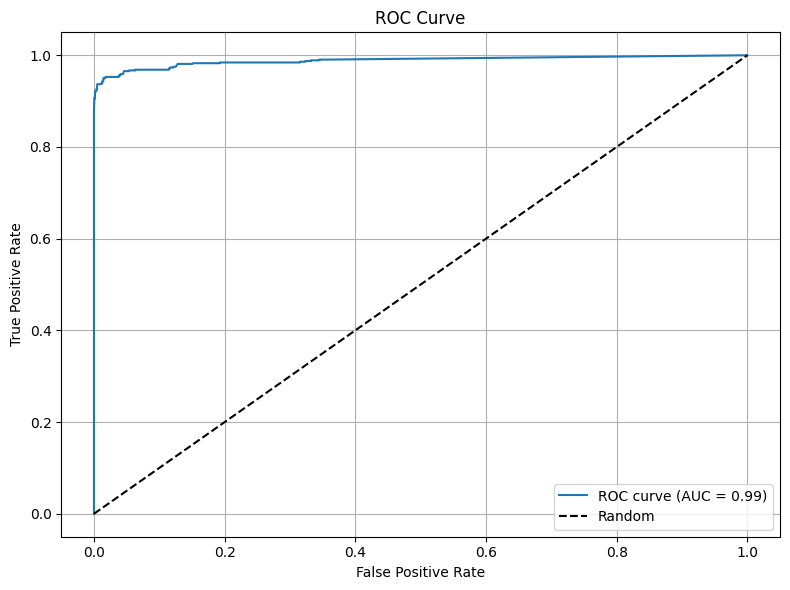

# ROC curve & AUC

fpr, tpr, thresholds = roc_curve(y_true, y_scores)

roc_auc = auc(fpr, tpr)

print(f"AUC : {roc_auc:.4f}")

# Plot ROC

plt.figure(figsize=(8, 6))

plt.plot(fpr, tpr, label=f'ROC curve (AUC = {roc_auc:.2f})')

plt.plot([0, 1], [0, 1], 'k--', label='Random')

plt.xlabel('False Positive Rate')

plt.ylabel('True Positive Rate')

plt.title('ROC Curve')

plt.legend(loc='lower right')

plt.grid(True)

plt.tight_layout()

plt.show()

Params: α=148.41, β=85.31, γ=0.08, δ=148.41

Confusion Matrix:

TN=4365, FP=0, FN=76, TP=559

Accuracy : 0.9848

Precision: 1.0000

Recall : 0.8803

AUC : 0.9884

# ----------------------

# Plots: Hit Rate & Attrition Over Full Simulation

# ----------------------

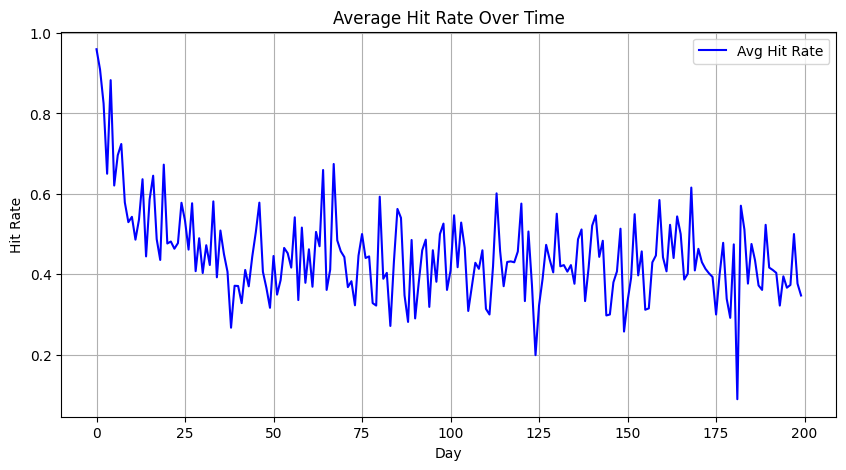

# Active-client hit rate over time

hit_rate_active = []

days = np.arange(T_tot)

for t in days:

act_clients = active_df.iloc[t]

active_ids = [int(col.split('_')[1]) for col, flag in act_clients.items() if flag]

daily = rfq_all[rfq_all['time'] == t]

rates = []

for cid in active_ids:

cr = daily[daily['client_id'] == cid]

if not cr.empty:

rates.append(cr['hit'].mean())

hit_rate_active.append(np.mean(rates) if rates else np.nan)

plt.figure(figsize=(10,5))

plt.plot(days, hit_rate_active, label='Avg Hit Rate', color='blue')

plt.title('Average Hit Rate Over Time')

plt.xlabel('Day'); plt.ylabel('Hit Rate'); plt.grid(True); plt.legend()

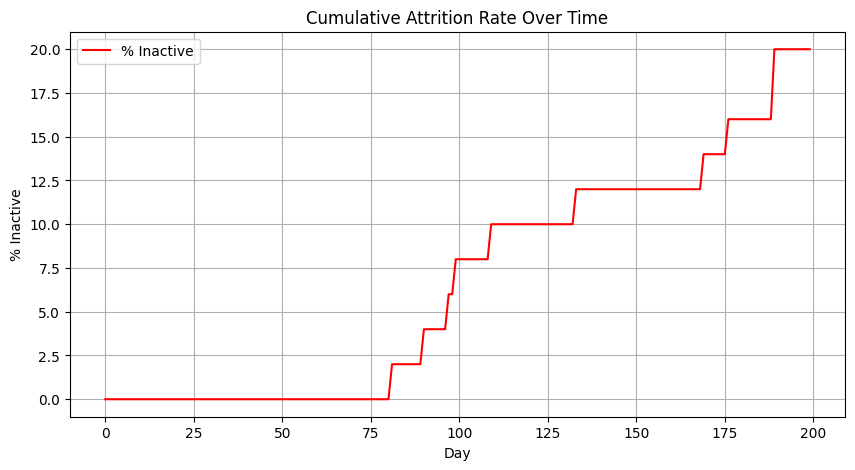

# Attrition rate over time

attr_rate = [100 * (Y_all.shape[1] - x) / Y_all.shape[1] for x in active_all]

plt.figure(figsize=(10,5))

plt.plot(days, attr_rate, label='% Inactive', color='red')

plt.title('Cumulative Attrition Rate Over Time')

plt.xlabel('Day'); plt.ylabel('% Inactive'); plt.grid(True); plt.legend();

# ----------------------

# Model Fit Visualization

# ----------------------

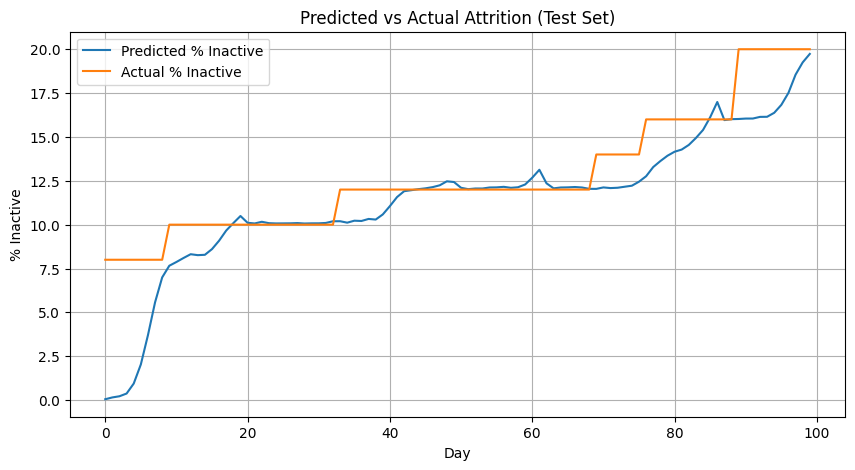

# Compare predicted attrition vs actual on test

pred_rate = risk_df.groupby('time')['p_inactive'].mean()

actual_rate = [100*(N_clients-x)/N_clients for x in active_test]

plt.figure(figsize=(10,5))

plt.plot(pred_rate.index, 100*pred_rate.values, label='Predicted % Inactive')

plt.plot(actual_rate, label='Actual % Inactive')

plt.title('Predicted vs Actual Attrition (Test Set)')

plt.xlabel('Day'); plt.ylabel('% Inactive'); plt.legend(); plt.grid(True)

import numpy as np

import matplotlib.pyplot as plt

# ----------------------

# Function: Plot Clients by ID (single figure with subplots)

# ----------------------

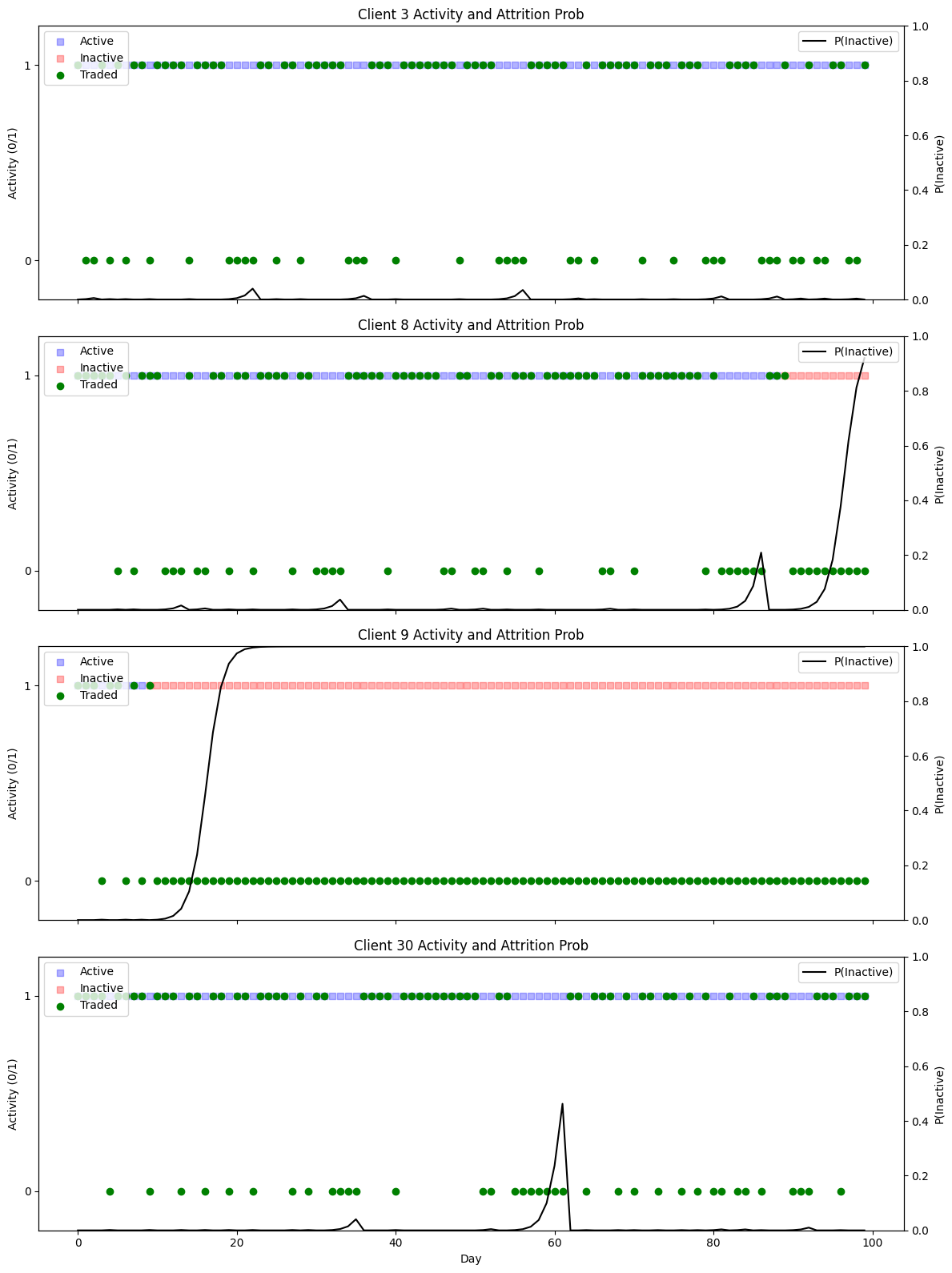

def plot_clients_subplots(client_ids):

"""

For each client in client_ids, create a subplot in one figure:

- Left y-axis: active (blue=active, red=inactive) and trading days (green), with numeric ticks (0/1)

- Right y-axis: attrition probability over time

- Separate legends: left for 'Active', 'Inactive', 'Traded'; right for 'P(Inactive)'

- Title of each subplot shows the client ID

"""

n = len(client_ids)

fig, axes = plt.subplots(nrows=n, ncols=1, figsize=(12, 4*n), sharex=True)

if n == 1:

axes = [axes]

days = np.arange(T_test)

for ax1, cid in zip(axes, client_ids):

# gather P(inactive) values

p_vals = [

risk_df.loc[

(risk_df['client_id'] == cid) & (risk_df['time'] == t),

'p_inactive'

].item()

for t in days

]

# latent active flags and trading days

active_flag = active_df[T_train:][f'client_{cid}'].values

trade_days = Y_test.iloc[:, cid]

# Left axis: Active vs Inactive

idx_active = days[active_flag]

idx_inactive = days[~active_flag]

h_active = ax1.scatter(idx_active, [1]*len(idx_active), c='blue', marker='s', alpha=0.3, label='Active')

h_inactive = ax1.scatter(idx_inactive, [1]*len(idx_inactive), c='red', marker='s', alpha=0.3, label='Inactive')

# Left axis: actual trades (0 or 1)

h_trade = ax1.scatter(trade_days.index, trade_days.values,

c='green', marker='o', label='Traded')

# Set numeric ticks on left y-axis

ax1.set_ylim(-0.2, 1.2)

ax1.set_yticks([0, 1])

ax1.set_ylabel('Activity (0/1)')

ax1.set_title(f'Client {cid} Activity and Attrition Prob')

# Left-axis legend

ax1.legend(handles=[h_active, h_inactive, h_trade],

labels=['Active', 'Inactive', 'Traded'],

loc='upper left')

# Right axis: P(Inactive)

ax2 = ax1.twinx()

h_prob, = ax2.plot(days, p_vals, c='black', label='P(Inactive)')

ax2.set_ylim(0, 1)

ax2.set_ylabel('P(Inactive)')

# Right-axis legend

ax2.legend(handles=[h_prob], loc='upper right')

axes[-1].set_xlabel('Day')

plt.tight_layout()

plt.show()

# Example: plot select clients in one figure

#plot_clients_subplots([3, 8, 9, 18])

plot_clients_subplots([3, 8, 9, 30])

Simulation of client abnormal behavior¶

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from scipy.stats import poisson, norm

from collections import deque

def run_simulation(N_clients=50,

T=200,

reservation_price_mean=100,

reservation_price_std_pct=0.1,

lambda_mean=1,

lambda_std=0.05,

prior_mean=60,

prior_std=10,

reservation_price_noise_std=None,

discount_trigger_pct=0.35, # trigger threshold: 0.5 means 50% lower

boosted_rate_factor = 10,

hit_rate_target=0.4,

window_size=10,

attrition_threshold=0.1,

random_seed=42):

"""

Simulate RFQ interactions with Bayesian quantile pricing and client attrition.

Adds a mechanism: if a client gets a quote at least `discount_trigger_pct` below their reservation price,

they double their RFQ rate until the dealer quotes above their reservation price.

"""

np.random.seed(random_seed)

# Generate distribution of reservation prices

reservation_prices = np.random.normal(reservation_price_mean,

reservation_price_mean * reservation_price_std_pct,

N_clients)

# Noise in reservation prices

fair_price = reservation_price_mean

res_price_noise_std = reservation_price_noise_std or (fair_price * reservation_price_std_pct * 2)

res_price_noise_var = res_price_noise_std ** 2

# Base RfQ intensities

lambdas = np.abs(np.random.normal(lambda_mean, lambda_std, N_clients))

base_lambdas = lambdas.copy() # store for reset later

# Posterior beliefs

clients_posterior = {i: {'mean': prior_mean, 'var': prior_std ** 2,

'n': 0, 'sum_obs': 0.0}

for i in range(N_clients)}

z = norm.ppf(1 - hit_rate_target)

active = np.ones(N_clients, dtype=bool)

# Flags for tracking "boosted" mode

boosted = np.zeros(N_clients, dtype=bool)

# Track daily active/boosted status

active_flags = np.zeros((T, N_clients), dtype=bool)

boosted_flags = np.zeros((T, N_clients), dtype=bool)

daily_history = [deque(maxlen=window_size) for _ in range(N_clients)]

active_history = []

records = []

Y = np.zeros((T, N_clients), dtype=int) # binary: whether client sent at least one RFQ that day

for t in range(T):

daily_hits = np.zeros(N_clients, dtype=int)

daily_reqs = np.zeros(N_clients, dtype=int)

for i in range(N_clients):

if not active[i]:

continue

n_rfq = poisson.rvs(lambdas[i])

if n_rfq > 0:

Y[t, i] = 1

for _ in range(n_rfq):

post = clients_posterior[i]

price = max(0.0, post['mean'] + np.sqrt(post['var'] + res_price_noise_var) * z)

r = norm.rvs(reservation_prices[i], res_price_noise_std)

# Trading happens when price <= reservation price

hit = price <= r

daily_reqs[i] += 1

daily_hits[i] += int(hit)

# Check discount trigger

if price <= (1 - discount_trigger_pct) * r:

boosted[i] = True

lambdas[i] = base_lambdas[i] * boosted_rate_factor

elif boosted[i] and price > r / (1-discount_trigger_pct):

boosted[i] = False

lambdas[i] = base_lambdas[i]

# Update posterior belief

post['n'] += 1

post['sum_obs'] += r

post_var = 1 / (1 / (prior_std ** 2) + post['n'] / res_price_noise_var)

post['var'] = post_var

post['mean'] = post_var * (prior_mean / (prior_std ** 2) +

post['sum_obs'] / res_price_noise_var)

records.append({'time': t,

'client_id': i,

'price': price,

'reservation': r,

'hit': hit,

'boosted': boosted[i]})

# Update attrition status

for i in range(N_clients):

if not active[i] or daily_reqs[i] == 0:

continue

rate = daily_hits[i] / daily_reqs[i]

daily_history[i].append(rate)

if len(daily_history[i]) == window_size and np.mean(daily_history[i]) < attrition_threshold:

active[i] = False

active_history.append(int(active.sum()))

active_flags[t, :] = active.copy()

boosted_flags[t, :] = boosted.copy()

rfq_df = pd.DataFrame(records)

activity_df = pd.DataFrame(Y, columns=[f'client_{i}' for i in range(N_clients)])

active_df = pd.DataFrame(active_flags, columns=[f'client_{i}' for i in range(N_clients)])

boosted_df = pd.DataFrame(boosted_flags, columns=[f'client_{i}' for i in range(N_clients)])

return rfq_df, active_history, activity_df, active_df, boosted_df

# Run simulation

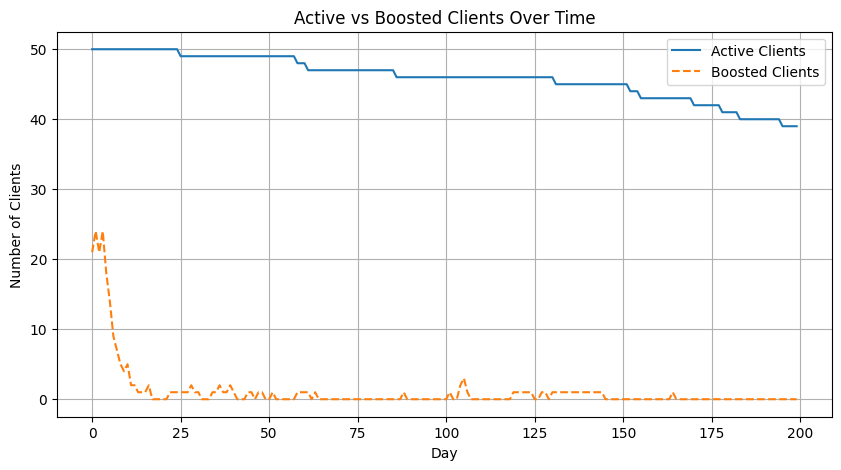

rfq_df, active_history, activity_df, active_df, boosted_df = run_simulation()

# Plot active and boosted clients over time

plt.figure(figsize=(10,5))

plt.plot(active_df.sum(axis=1), label='Active Clients')

plt.plot(boosted_df.sum(axis=1), label='Boosted Clients', linestyle='--')

plt.xlabel('Day')

plt.ylabel('Number of Clients')

plt.title('Active vs Boosted Clients Over Time')

plt.legend()

plt.grid(True)

plt.show()

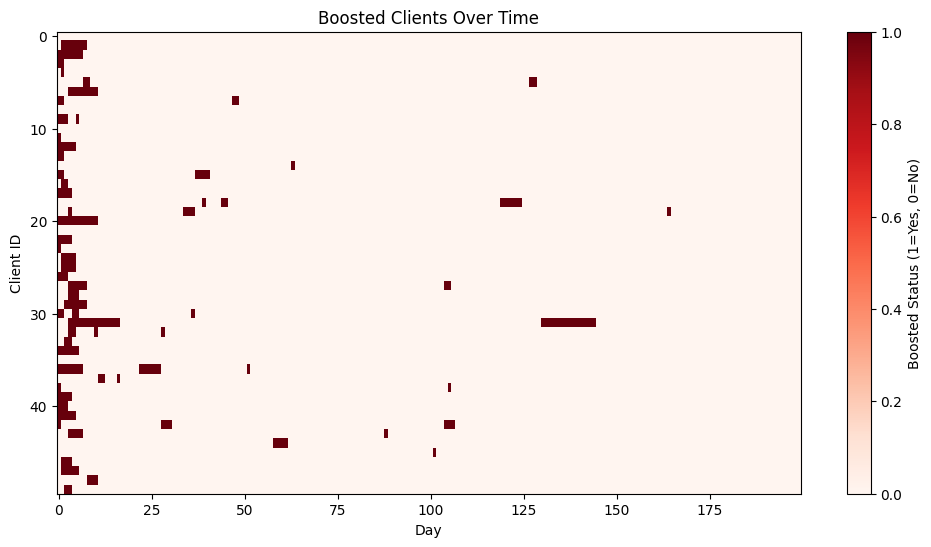

# Heatmap of boosted status

plt.figure(figsize=(12,6))

plt.imshow(boosted_df.T, aspect='auto', cmap='Reds')

plt.colorbar(label='Boosted Status (1=Yes, 0=No)')

plt.xlabel('Day')

plt.ylabel('Client ID')

plt.title('Boosted Clients Over Time')

plt.show()

from scipy.special import betaln, gammaln

from scipy.optimize import minimize

# -----------------------------

# Beta-Binomial mixture MLE with shared mean

# -----------------------------

def log_beta_binom_pmf(x, n, alpha, beta):

# log [ C(n,x) * B(alpha+x, beta+n-x) / B(alpha,beta) ]

return (

gammaln(n + 1) - gammaln(x + 1) - gammaln(n - x + 1)

+ betaln(alpha + x, beta + n - x)

- betaln(alpha, beta)

)

def neg_log_likelihood(params, xs, ns):

# params = [logit_mu, log_k_g, log_k_b, logit_qg]

logit_mu, log_k_g, log_k_b, logit_qg = params

mu = 1 / (1 + np.exp(-logit_mu)) # shared mean

k_g = np.exp(log_k_g) + 1e-8

k_b = np.exp(log_k_b) + 1e-8

qg = 1 / (1 + np.exp(-logit_qg))

# convert to alpha, beta

alpha_g, beta_g = mu * k_g, (1 - mu) * k_g

alpha_b, beta_b = mu * k_b, (1 - mu) * k_b

# mixture likelihood per client

ll = []

for x, n in zip(xs, ns):

log_p_g = log_beta_binom_pmf(x, n, alpha_g, beta_g)

log_p_b = log_beta_binom_pmf(x, n, alpha_b, beta_b)

# log-sum-exp for mixture

a = np.log(qg) + log_p_g

b = np.log(1 - qg) + log_p_b

m = max(a, b)

ll_i = m + np.log(np.exp(a - m) + np.exp(b - m))

ll.append(ll_i)

return -np.sum(ll)

def fit_beta_mixture_mle(activity_df, train_days):

"""

activity_df: (T x N) binary DataFrame

train_days: number of days used for training (first half)

Returns dict with fitted parameters.

"""

T, N = activity_df.shape

A = activity_df.iloc[:train_days].values # (train_days x N)

xs = A.sum(axis=0) # successes per client in training

ns = np.full_like(xs, fill_value=train_days)

# rough start for mean

p_hat = xs.mean() / train_days

logit_mu0 = np.log(p_hat / (1 - p_hat + 1e-8))

start = np.array([

logit_mu0,

np.log(10.0), # k_g initial concentration

np.log(2.0), # k_b initial concentration

0.0 # logit(0.5)

], dtype=float)

res = minimize(neg_log_likelihood, start, args=(xs, ns), method='L-BFGS-B')

logit_mu, log_k_g, log_k_b, logit_qg = res.x

mu = 1 / (1 + np.exp(-logit_mu))

k_g = np.exp(log_k_g) + 1e-8

k_b = np.exp(log_k_b) + 1e-8

params = {

'mu': float(mu),

'alpha_g': float(mu * k_g), 'beta_g': float((1 - mu) * k_g),

'alpha_b': float(mu * k_b), 'beta_b': float((1 - mu) * k_b),

'q_g': float(1 / (1 + np.exp(-logit_qg))),

'success': bool(res.success),

'message': res.message

}

return params

def posterior_good(x, n, params):

a_g = params['alpha_g']; b_g = params['beta_g']

a_b = params['alpha_b']; b_b = params['beta_b']

q_g = params['q_g']

log_p_g = log_beta_binom_pmf(x, n, a_g, b_g)

log_p_b = log_beta_binom_pmf(x, n, a_b, b_b)

a = np.log(q_g) + log_p_g

b = np.log(1 - q_g) + log_p_b

m = max(a, b)

num = np.exp(a - m)

den = num + np.exp(b - m)

return float(num / den)

# Fit on first half, removing first 25 days until it settles

T = activity_df.shape[0]

mid = T // 2

params = fit_beta_mixture_mle(activity_df[25:], train_days=mid)

# Detect abnormalities on second half using a sliding window

n_window = 10 # window size for detection, can be adjusted

threshold = 0.5 # classify as abnormal if p(good|D) < threshold

N = activity_df.shape[1]

abnormal_flags = np.zeros_like(activity_df.values, dtype=bool)

# For each day t in the second half, use the last n_window days (bounded within the second half)

for t in range(mid, T):

start = max(mid, t - n_window + 1)

end = t + 1

window = activity_df.iloc[start:end].values # (w x N)

n = window.shape[0]

x = window.sum(axis=0)

# Posterior for each client

p_good = np.array([posterior_good(int(xi), int(n), params) for xi in x])

abnormal_flags[t, :] = p_good < threshold

abnormal_df = pd.DataFrame(abnormal_flags, columns=activity_df.columns, index=activity_df.index)

params{'mu': 0.6459024041525655,

'alpha_g': 17819.14219878137,

'beta_g': 9768.837168102045,

'alpha_b': 0.6772910514791353,

'beta_b': 0.3713055277018204,

'q_g': 0.892871535754001,

'success': True,

'message': 'CONVERGENCE: REL_REDUCTION_OF_F_<=_FACTR*EPSMCH'}import numpy as np

import matplotlib.pyplot as plt

from scipy.stats import beta

def plot_fitted_betas(params, bins=200):

"""

Plot fitted good vs bad Beta distributions.

params: dict returned by fit_beta_mixture_mle

"""

a_g, b_g = params['alpha_g'], params['beta_g']

a_b, b_b = params['alpha_b'], params['beta_b']

q_g = params['q_g']

# Grid

x = np.linspace(0, 1, bins)

# Densities

pdf_g = beta.pdf(x, a_g, b_g)

pdf_b = beta.pdf(x, a_b, b_b)

plt.figure(figsize=(10, 6))

plt.plot(x, pdf_g, label=f"Good (α={a_g:.2f}, β={b_g:.2f})", lw=2, color="blue")

plt.plot(x, pdf_b, label=f"Bad (α={a_b:.2f}, β={b_b:.2f})", lw=2, color="red")

plt.fill_between(x, pdf_g, alpha=0.2, color="blue")

plt.fill_between(x, pdf_b, alpha=0.2, color="red")

plt.title("Fitted Beta Distributions (Good vs Bad)")

plt.xlabel("Success probability")

plt.ylabel("Density")

plt.legend()

plt.grid(True, ls="--", alpha=0.5)

plt.show()

plot_fitted_betas(params)

# Use a previous window (exclude day t) when computing P(good|D)

n_window = 10

threshold = 0.5

def build_pgood_panel(activity_df, boosted_df, active_df, params, mid, n_window, threshold):

T, N = activity_df.shape

rows = []

# Start at mid + n_window to ensure a full *previous* window exists

for t in range(mid + n_window, T):

start = t - n_window

end = t # exclude day t

window = activity_df.iloc[start:end] # (n_window x N)

x = window.sum(axis=0).values.astype(int) # successes per client in previous window

n = n_window

# compute p_good for each client

p_goods = []

for j in range(N):

p = posterior_good(int(x[j]), int(n), params)

p_goods.append(p)

p_goods = np.array(p_goods)

# flags at time t

boosted_t = boosted_df.iloc[t].values.astype(bool)

active_t = active_df.iloc[t].values.astype(bool)

inactive_t = ~active_t

traded_today = activity_df.iloc[t].values.astype(int)

for j in range(N):

rows.append({

'day': t,

'client_id': j,

'x': int(x[j]),

'n': int(n),

'p_good': float(p_goods[j]),

'abnormal': bool(p_goods[j] < threshold),

'boosted': bool(boosted_t[j]),

'inactive': bool(inactive_t[j]),

'traded_today': int(traded_today[j])

})

panel = pd.DataFrame(rows)

return panel

panel_df = build_pgood_panel(activity_df, boosted_df, active_df, params, mid, n_window, threshold)

# Correctly aligned daily summary for second half *with windowing*

days = sorted(panel_df['day'].unique())

daily_summary = panel_df.groupby('day').agg(

abnormal_count=('abnormal', 'sum'),

boosted_count=('boosted', 'sum'),

inactive_count=('inactive', 'sum')

).reset_index()

# Overlap summary on client-day panel

overlap_summary = {

'days_evaluated': int(len(days)),

'clients': int(N),

'total_client_days': int(panel_df.shape[0]),

'abnormal_client_days': int(panel_df['abnormal'].sum()),

'boosted_client_days': int(panel_df['boosted'].sum()),

'inactive_client_days': int(panel_df['inactive'].sum()),

'abnormal_and_boosted': int((panel_df['abnormal'] & panel_df['boosted']).sum()),

'abnormal_and_inactive': int((panel_df['abnormal'] & panel_df['inactive']).sum()),

'abnormal_not_boosted_or_inactive': int((panel_df['abnormal'] & ~panel_df['boosted'] & ~panel_df['inactive']).sum())

}

overlap_df2 = pd.DataFrame([overlap_summary])

# Heatmap of p_good by client (days x clients) for visual inspection

# Build a matrix with rows=days, cols=clients

days_idx = daily_summary['day'].values

pgood_mat = np.full((len(days_idx), N), np.nan)

for i, t in enumerate(days_idx):

slice_t = panel_df[panel_df['day'] == t].sort_values('client_id')

pgood_mat[i, :] = slice_t['p_good'].values

plt.figure(figsize=(12,6))

plt.imshow(pgood_mat.T, aspect='auto')

plt.colorbar(label='P(good | previous window)')

plt.xlabel('Day index in second half')

plt.ylabel('Client ID')

plt.title('Per-client P(good|D) over time (previous window)')

plt.show()

from matplotlib.lines import Line2D

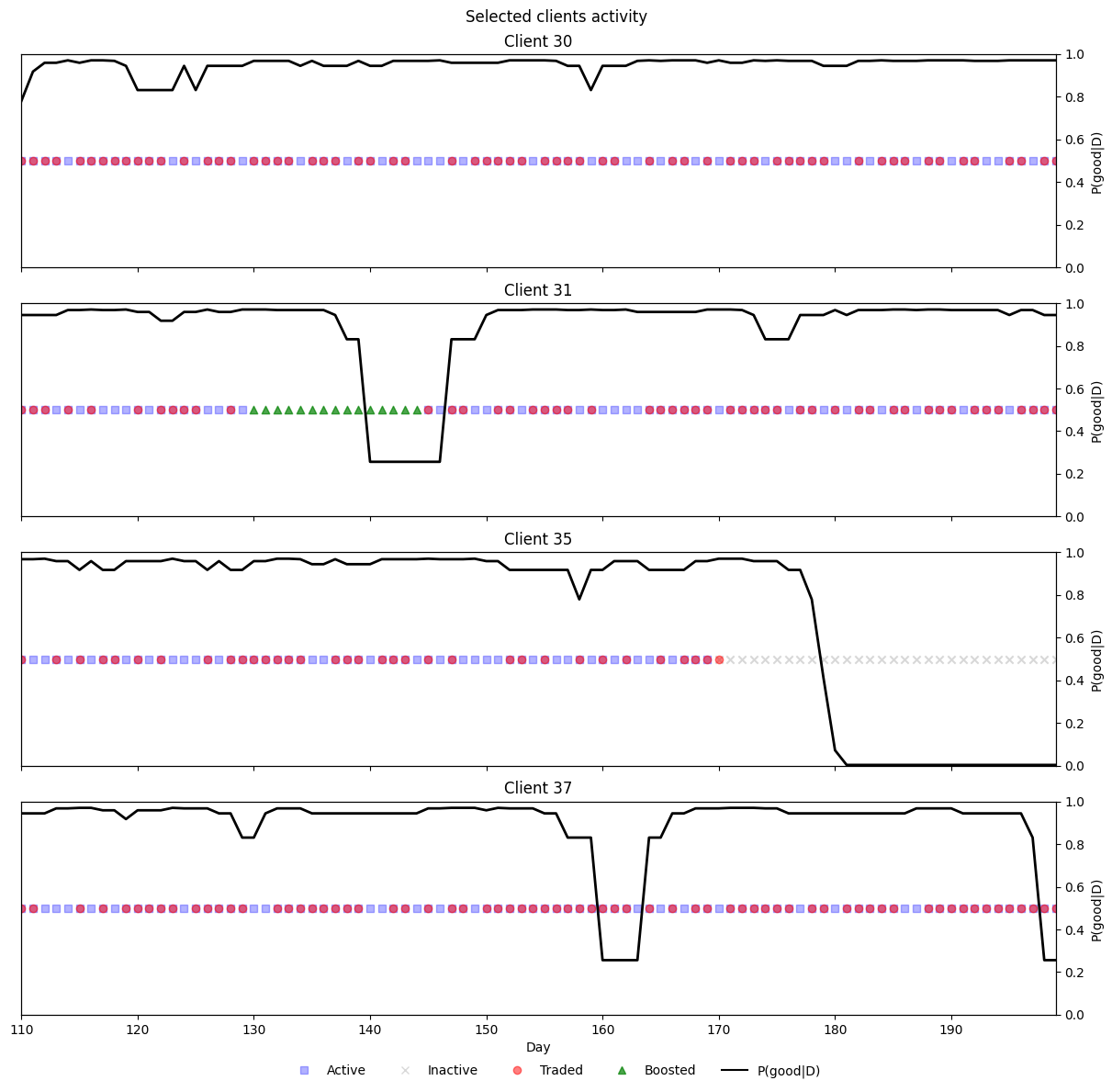

def plot_clients_activity_prob(clients, df):

"""

One figure with one row per client.

On boosted days, only the 'Boosted' marker is shown (others hidden).

"""

clients = list(clients)

n = len(clients)

if n == 0:

return

fig, axes = plt.subplots(n, 1, figsize=(12, 2.8 * n), sharex=True, constrained_layout=True)

if n == 1:

axes = [axes]

# Build a single, global legend

legend_elems = [

Line2D([0],[0], marker='s', linestyle='None', color='blue', alpha=0.3, label='Active'),

Line2D([0],[0], marker='x', linestyle='None', color='gray', alpha=0.3, label='Inactive'),

Line2D([0],[0], marker='o', linestyle='None', color='red', alpha=0.5, label='Traded'),

Line2D([0],[0], marker='^', linestyle='None', color='green', alpha=0.7, label='Boosted'),

Line2D([0],[0], linestyle='-', color='black', label='P(good|D)'),

]

x_min, x_max = None, None

for ax, cid in zip(axes, clients):

df_c = df[df['client_id'] == cid].sort_values('day').copy()

if df_c.empty:

ax.set_title(f"Client {cid} (no data)")

ax.set_yticks([])

continue

# Masks

boosted_mask = df_c['boosted']

active_mask = (~df_c['inactive']) & (~boosted_mask)

inactive_mask = df_c['inactive'] & (~boosted_mask)

traded_mask = (df_c['traded_today'] == 1) & (~boosted_mask)

# Scatter statuses

ax.scatter(df_c['day'][active_mask], [1]*active_mask.sum(), c='blue', marker='s', alpha=0.3)

ax.scatter(df_c['day'][inactive_mask], [1]*inactive_mask.sum(), c='gray', marker='x', alpha=0.3)

ax.scatter(df_c['day'][traded_mask], [1]*traded_mask.sum(), c='red', marker='o', alpha=0.5)

ax.scatter(df_c['day'][boosted_mask], [1]*boosted_mask.sum(), c='green', marker='^', alpha=0.7, zorder=3)

ax.set_yticks([])

ax.set_ylim(0.5, 1.5)

# p_good

ax2 = ax.twinx()

ax2.plot(df_c['day'], df_c['p_good'], color='black', lw=2)

ax2.set_ylim(0, 1)

ax2.set_ylabel("P(good|D)")

ax.set_title(f"Client {cid}")

# Track x-lims

dmin, dmax = df_c['day'].min(), df_c['day'].max()

x_min = dmin if x_min is None else min(x_min, dmin)

x_max = dmax if x_max is None else max(x_max, dmax)

axes[-1].set_xlabel("Day")

if x_min is not None and x_max is not None:

axes[-1].set_xlim(x_min, x_max)

fig.suptitle("Selected clients activity", y=1.02)

# Move legend below figure

fig.legend(handles=legend_elems, loc='lower center', ncol=5, frameon=False, bbox_to_anchor=(0.5, -0.03))

plt.show()

plot_clients_activity_prob([30,31,35, 37], panel_df)

from sklearn.metrics import confusion_matrix

def _cm_df(cm, labels=("Pred 0", "Pred 1"), index=("True 0", "True 1")):

"""Pretty dataframe for a 2x2 confusion matrix."""

return pd.DataFrame(cm, index=index, columns=labels)

def evaluate_confusions(panel_df, normalize=False):

"""

Evaluate confusion matrices without recomputing thresholds.

Uses:

- df['abnormal'] as the model's predicted abnormal label (already thresholded).

- df['inactive'] and df['boosted'] as operational labels.

- Global abnormality = (inactive OR boosted).

Returns dict with both raw arrays and pretty DataFrames.

Set normalize=True to return per-true-class rates instead of counts.

"""

df = panel_df.copy()

# Ensure ints

y_abnormal = df["abnormal"].astype(int).values

y_inactive = df["inactive"].astype(int).values

y_boosted = df["boosted"].astype(int).values

# Global abnormality (prediction-side for the overall CM)

y_global_abn = (df["inactive"] | df["boosted"]).astype(int).values

# Normalization mode for sklearn

norm_mode = "true" if normalize else None

results = {}

# 1) Inactive (truth) vs Abnormal (model)

cm_inactive = confusion_matrix(y_inactive, y_abnormal, labels=[0,1], normalize=norm_mode)

results["inactive_vs_abnormal"] = cm_inactive

results["inactive_vs_abnormal_df"] = _cm_df(cm_inactive)

# 2) Boosted (truth) vs Abnormal (model)

cm_boosted = confusion_matrix(y_boosted, y_abnormal, labels=[0,1], normalize=norm_mode)

results["boosted_vs_abnormal"] = cm_boosted

results["boosted_vs_abnormal_df"] = _cm_df(cm_boosted)

# 3) OVERALL: Abnormal (truth) vs Global abnormality (prediction = inactive OR boosted)

cm_overall = confusion_matrix(y_abnormal, y_global_abn, labels=[0,1], normalize=norm_mode)

results["overall_abnormal_vs_global"] = cm_overall

results["overall_abnormal_vs_global_df"] = _cm_df(cm_overall)

return results

# Example usage:

cm_results = evaluate_confusions(panel_df, normalize=False)

print("Inactive (truth) vs Abnormal (model):\n", cm_results["inactive_vs_abnormal_df"], "\n")

print("Boosted (truth) vs Abnormal (model):\n", cm_results["boosted_vs_abnormal_df"], "\n")

print("Overall: Abnormal (truth) vs Global (inactive OR boosted) prediction:\n", cm_results["overall_abnormal_vs_global_df"])Inactive (truth) vs Abnormal (model):

Pred 0 Pred 1

True 0 3830 74

True 1 56 540

Boosted (truth) vs Abnormal (model):

Pred 0 Pred 1

True 0 3867 609

True 1 19 5

Overall: Abnormal (truth) vs Global (inactive OR boosted) prediction:

Pred 0 Pred 1

True 0 3811 75

True 1 69 545