import numpy as np

import matplotlib.pyplot as plt

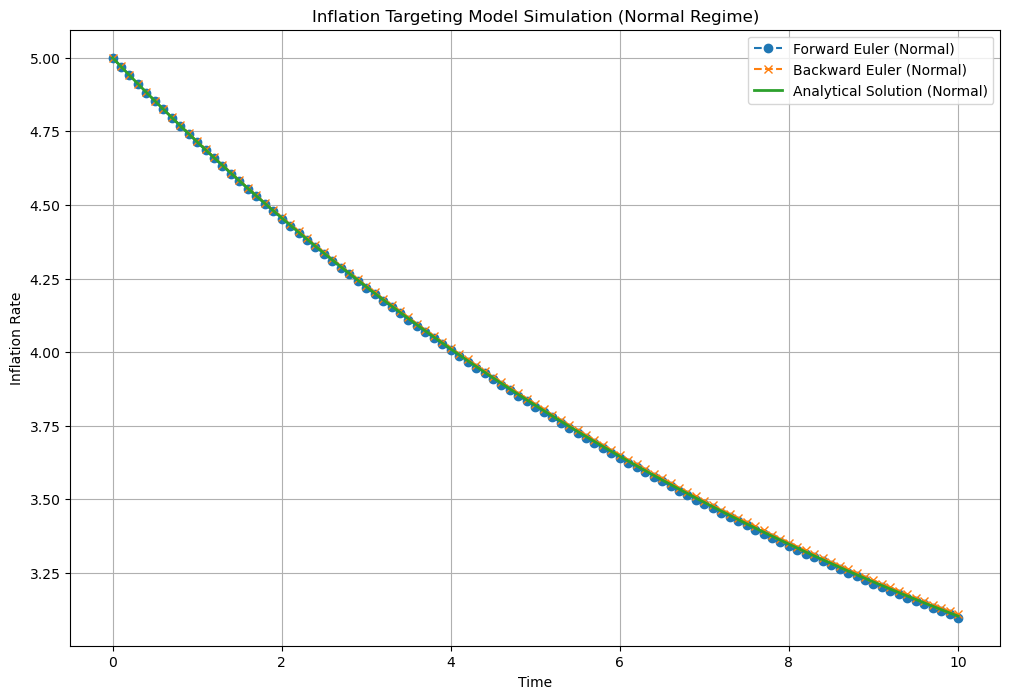

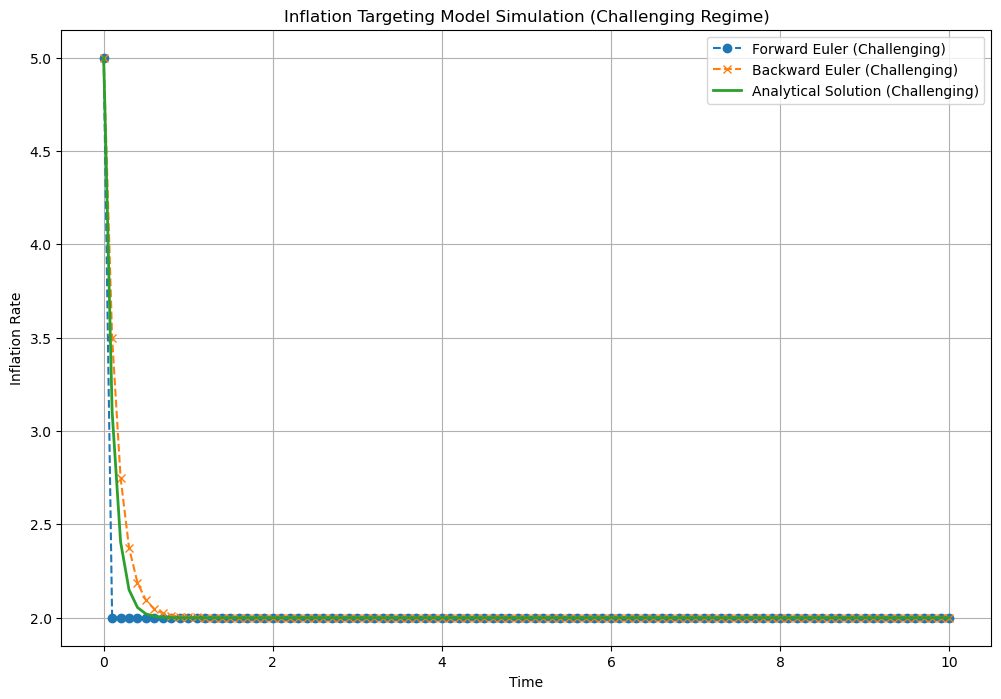

def simulate_inflation(theta, pi_hat, pi_t0, Delta, N):

# Time grid

time = np.linspace(0, N * Delta, N + 1)

# Arrays to store the results

pi_forward = np.zeros(N + 1)

pi_backward = np.zeros(N + 1)

pi_analytical = np.zeros(N + 1)

# Initial condition

pi_forward[0] = pi_t0

pi_backward[0] = pi_t0

# Analytical Solution

pi_analytical = pi_hat + (pi_t0 - pi_hat) * np.exp(-theta * time)

# Forward Euler Scheme

for i in range(N):

pi_forward[i + 1] = pi_forward[i] + Delta * theta * (pi_hat - pi_forward[i])

# Backward Euler Scheme

for i in range(N):

pi_backward[i + 1] = (pi_backward[i] + Delta * theta * pi_hat) / (1 + Delta * theta)

return time, pi_forward, pi_backward, pi_analytical

# Parameters for normal regime

theta_normal = 0.1

Delta_normal = 0.1

pi_hat = 2.0

pi_t0 = 5.0

N = 100

# Parameters for challenging regime

theta_challenging = 10.0

Delta_challenging = 0.1

# Simulate for normal regime

time_normal, pi_forward_normal, pi_backward_normal, pi_analytical_normal = simulate_inflation(

theta_normal, pi_hat, pi_t0, Delta_normal, N)

# Simulate for challenging regime

time_challenging, pi_forward_challenging, pi_backward_challenging, pi_analytical_challenging = simulate_inflation(

theta_challenging, pi_hat, pi_t0, Delta_challenging, N)

# Plot the results for normal regime

plt.figure(figsize=(12, 8))

plt.plot(time_normal, pi_forward_normal, label='Forward Euler (Normal)', marker='o', linestyle='--')

plt.plot(time_normal, pi_backward_normal, label='Backward Euler (Normal)', marker='x', linestyle='--')

plt.plot(time_normal, pi_analytical_normal, label='Analytical Solution (Normal)', linestyle='-', linewidth=2)

plt.xlabel('Time')

plt.ylabel('Inflation Rate')

plt.title('Inflation Targeting Model Simulation (Normal Regime)')

plt.legend()

plt.grid(True)

plt.show()

# Plot the results for challenging regime

plt.figure(figsize=(12, 8))

plt.plot(time_challenging, pi_forward_challenging, label='Forward Euler (Challenging)', marker='o', linestyle='--')

plt.plot(time_challenging, pi_backward_challenging, label='Backward Euler (Challenging)', marker='x', linestyle='--')

plt.plot(time_challenging, pi_analytical_challenging, label='Analytical Solution (Challenging)', linestyle='-', linewidth=2)

plt.xlabel('Time')

plt.ylabel('Inflation Rate')

plt.title('Inflation Targeting Model Simulation (Challenging Regime)')

plt.legend()

plt.grid(True)

plt.show()

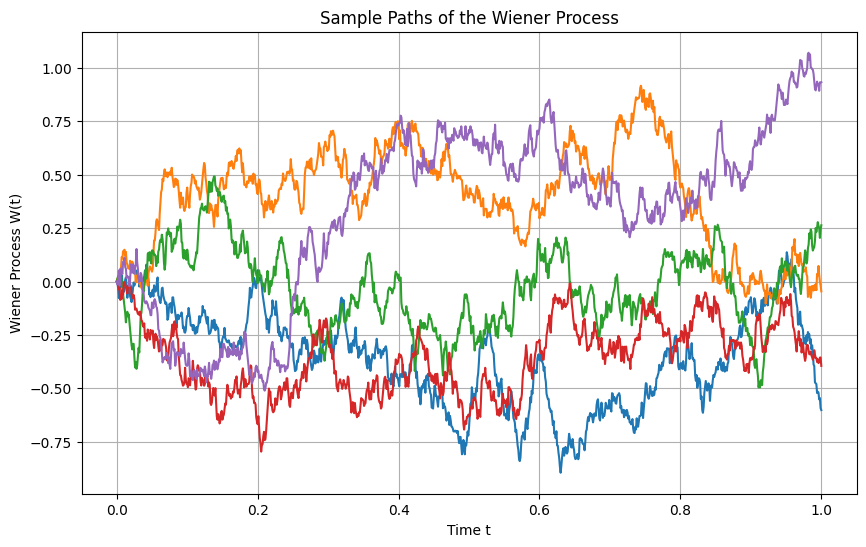

import matplotlib.pyplot as plt

import numpy as np

# Set the parameters for the Wiener process

T = 1.0 # total time

n = 1000 # number of steps

dt = T / n # time increment

t = np.linspace(0, T, n+1) # time points

# Number of paths to simulate

num_paths = 5

# Set up the plot

plt.figure(figsize=(10, 6))

# Simulate multiple paths

for _ in range(num_paths):

W = np.zeros(n+1) # Initialize the Wiener process for each path

for i in range(n):

W[i+1] = W[i] + np.sqrt(dt) * np.random.randn()

plt.plot(t, W, label=f'Path {_+1}')

# Customize the plot

plt.title('Sample Paths of the Wiener Process')

plt.xlabel('Time t')

plt.ylabel('Wiener Process W(t)')

plt.grid(True)

# Show the plot

plt.show()

Simulation using Gaussian processes¶

import GPy

import numpy as np

import matplotlib.pyplot as plt

# Time points at which to sample the Wiener process

t = np.linspace(0, 1, 1000).reshape(-1, 1)

# Define the Brownian motion kernel

brownian_kernel = GPy.kern.Brownian(input_dim=1, variance=1.0)

# Create a GP model with zero mean function

mean_function = GPy.mappings.Constant(input_dim=1, output_dim=1, value=0)

model = GPy.models.GPRegression(t, np.zeros_like(t), kernel=brownian_kernel, mean_function=mean_function)

# Ensure correct model optimization

model.optimize()

# Sample paths from the GP model

num_samples = 5

samples = model.posterior_samples_f(t, size=num_samples)

# Plot the sampled paths

plt.figure(figsize=(10, 6))

for i in range(num_samples):

plt.plot(t, samples[:, :, i], label=f'Sample {i+1}')

plt.title('Sampled Paths from a Wiener Process using Gaussian Processes')

plt.xlabel('Time')

plt.ylabel('W(t)')

plt.show()

import matplotlib.pyplot as plt

import numpy as np

# Set the parameters for Brownian motion with drift and volatility

T = 1.0 # total time

n = 1000 # number of steps

dt = T / n # time increment

t = np.linspace(0, T, n+1) # time points

# Brownian motion parameters

mu = 5 # drift

sigma = 2.0 # volatility

# Number of paths to simulate

num_paths = 5

# Set up the plot

plt.figure(figsize=(10, 6))

# Simulate multiple paths

for _ in range(num_paths):

X = np.zeros(n+1) # Initialize the process for each path

for i in range(n):

X[i+1] = X[i] + mu * dt + sigma * np.sqrt(dt) * np.random.randn()

plt.plot(t, X, label=f'Path {_+1}')

# Customize the plot

plt.title('Sample Paths of Brownian Motion with drift')

plt.xlabel('Time t')

plt.ylabel('X(t)')

plt.grid(True)

# Show the plot

plt.show()

Simulation using Gaussian Processes¶

import GPy

import numpy as np

import matplotlib.pyplot as plt

# Parameters for Brownian motion with drift

S0 = 0.0 # Initial value

mu = 0.5 # Drift coefficient

sigma = 0.3 # Volatility

T = 1.0 # Total time

n = 1000 # Number of steps

t = np.linspace(0, T, n+1).reshape(-1, 1) # Time points

# Define the custom kernel for Brownian motion

class BrownianMotionKernel(GPy.kern.Kern):

def __init__(self, input_dim, sigma=1.0, active_dims=None):

super(BrownianMotionKernel, self).__init__(input_dim, active_dims, 'Brownian')

self.sigma = GPy.core.Param('sigma', sigma)

self.link_parameters(self.sigma)

def K(self, X, X2=None):

if X2 is None:

X2 = X

t1 = X

t2 = X2.T

# Covariance function of Brownian motion: sigma^2 * min(s, t)

cov_matrix = self.sigma**2 * np.minimum(t1, t2)

return cov_matrix

def Kdiag(self, X):

return self.sigma**2 * X[:, 0]

# No-op for gradient update since we are not optimizing the kernel

def update_gradients_full(self, dL_dK, X, X2=None):

pass

# No-op for kernel gradient since we are not optimizing the kernel

def gradients_X(self, dL_dK, X, X2=None):

return np.zeros(X.shape)

# Custom mean function to include drift

class BrownianMotionMean(GPy.core.Mapping):

def __init__(self, input_dim, output_dim, S0=0.0, mu=0.0):

super(BrownianMotionMean, self).__init__(input_dim, output_dim)

self.S0 = S0 # Initial value

self.mu = mu # Drift coefficient

def f(self, X):

# Mean function: S0 + mu * t

return self.S0 + self.mu * X

def update_gradients(self, dL_df, X):

pass

def gradients_X(self, dL_df, X):

return np.zeros(X.shape)

# Instantiate the Brownian motion kernel with parameters

bm_kernel = BrownianMotionKernel(input_dim=1, sigma=sigma)

# Instantiate the mean function with S0 and mu

mean_function = BrownianMotionMean(input_dim=1, output_dim=1, S0=S0, mu=mu)

# Provide the initial observation at t=0

t_data = np.array([[0.0]])

Y_data = np.array([[S0]])

# Create a GP model with the custom mean function and Brownian motion kernel

model = GPy.models.GPRegression(t_data, Y_data, kernel=bm_kernel, mean_function=mean_function)

# Set noise variance to a negligible value since we're simulating without observation noise

model.likelihood.variance.fix(1e-10)

# Sample paths from the GP model

num_samples = 5

samples = model.posterior_samples_f(t, size=num_samples)

# Plot the sampled paths

plt.figure(figsize=(10, 6))

for i in range(num_samples):

plt.plot(t, samples[:, :, i], label=f'Path {i+1}')

plt.title(f'Sampled Paths from Brownian Motion with Drift')

plt.xlabel('Time t')

plt.ylabel('S(t)')

plt.grid(True)

plt.legend()

plt.show()

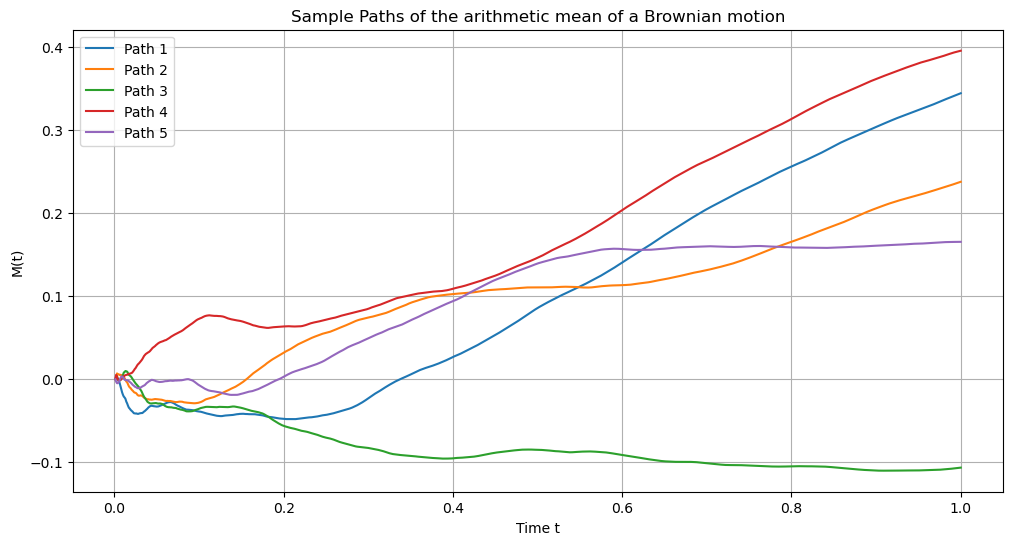

Arithmetic Average of the Brownian Motion¶

Simulation using discrete paths¶

import matplotlib.pyplot as plt

import numpy as np

# Set the parameters for Brownian motion with drift and volatility

T = 1.0 # total time

n = 1000 # number of steps

dt = T / n # time increment

t = np.linspace(dt, T, n) # time points starting from dt to avoid division by zero

# Brownian motion parameters

S0 = 0.0 # initial value of S_u

mu = 0.5 # drift coefficient

sigma = 0.3 # volatility

# Number of paths to simulate

num_paths = 5

# Initialize array to store M_t for each path

M_t_paths = np.zeros((n, num_paths))

# Set up the plot

plt.figure(figsize=(12, 6))

# Simulate multiple paths

for path in range(num_paths):

# Initialize S_u for each path

S = np.zeros(n + 1) # n+1 because we include S0

S[0] = S0

# Simulate S_u using Euler-Maruyama method

for i in range(n):

dW = np.sqrt(dt) * np.random.randn() # Brownian increment

S[i + 1] = S[i] + mu * dt + sigma * dW

# Compute cumulative sum to approximate the integral

cumulative_S = np.cumsum(S[:-1]) * dt # Exclude the last S[n+1]

# Compute M_t at each time point

M_t = cumulative_S / t

M_t_paths[:, path] = M_t

# Plot the path

plt.plot(t, M_t, label=f'Path {path + 1}')

# Customize the plot

plt.title('Sample Paths of the arithmetic mean of a Brownian motion')

plt.xlabel('Time t')

plt.ylabel('M(t)')

plt.grid(True)

plt.legend()

# Show the plot

plt.show()

Simulation using Gaussian Processes¶

import GPy

import numpy as np

import matplotlib.pyplot as plt

# Parameters for Brownian motion with drift

S0 = 0.0 # Initial value

mu = 0.5 # Drift coefficient

sigma = 0.3 # Volatility

T = 1.0 # Total time

n = 1000 # Number of steps

t = np.linspace(1e-6, T, n+1).reshape(-1, 1) # Time points, avoid t=0 to prevent division by zero

# Define the custom kernel based on the provided covariance function

class TimeAverageKernel(GPy.kern.Kern):

def __init__(self, input_dim, sigma=1.0, active_dims=None):

super(TimeAverageKernel, self).__init__(input_dim, active_dims, 'TimeAverage')

self.sigma = GPy.core.Param('sigma', sigma)

self.link_parameters(self.sigma)

def K(self, X, X2=None):

if X2 is None:

X2 = X

t1 = X[:, 0].reshape(-1, 1) # Column vector

t2 = X2[:, 0].reshape(1, -1) # Row vector

t_min = np.minimum(t1, t2)

t_max = np.maximum(t1, t2)

# Compute the covariance matrix using the given formula

cov_matrix = self.sigma ** 2 * (t_min / 2) * (1 - t_min / (3 * t_max))

return cov_matrix

def Kdiag(self, X):

t = X[:, 0]

# Compute the diagonal elements of the covariance matrix

cov_diag = self.sigma ** 2 * (t / 2) * (1 - t / (3 * t))

# Simplify the expression

cov_diag = self.sigma ** 2 * (t / 2) * (1 - 1 / 3)

cov_diag = self.sigma ** 2 * (t / 2) * (2 / 3)

cov_diag = self.sigma ** 2 * t * (1 / 3)

return cov_diag

def update_gradients_full(self, dL_dK, X, X2=None):

pass

def gradients_X(self, dL_dK, X, X2=None):

return np.zeros(X.shape)

# Custom mean function to include drift

class TimeAverageMean(GPy.core.Mapping):

def __init__(self, input_dim, output_dim, S0=0.0, mu=0.0):

super(TimeAverageMean, self).__init__(input_dim, output_dim)

self.S0 = S0 # Initial value

self.mu = mu # Drift coefficient

def f(self, X):

t = X[:, 0]

mean = self.S0 + 0.5 * self.mu * t

return mean.reshape(-1, 1)

def update_gradients(self, dL_df, X):

pass

def gradients_X(self, dL_df, X):

return np.zeros(X.shape)

# Instantiate the Time Average kernel with parameters

ta_kernel = TimeAverageKernel(input_dim=1, sigma=sigma)

# Instantiate the mean function with S0 and mu

mean_function = TimeAverageMean(input_dim=1, output_dim=1, S0=S0, mu=mu)

# Provide the initial observation at t=1e-6 (approaching zero)

t_data = np.array([[1e-6]])

Y_data = mean_function.f(t_data) # Mean at t=1e-6

# Create a GP model with the custom mean function and Time Average kernel

model = GPy.models.GPRegression(t_data, Y_data, kernel=ta_kernel, mean_function=mean_function)

# Set noise variance to a negligible value since we're simulating without observation noise

model.likelihood.variance.fix(1e-10)

# Sample paths from the GP model

num_samples = 5

samples = model.posterior_samples_f(t, size=num_samples)

# Plot the sampled paths

plt.figure(figsize=(12, 6))

for i in range(num_samples):

plt.plot(t, samples[:, :, i], label=f'Path {i+1}')

plt.title('Sampled Paths of the arithmetic mean of a Brownian motion')

plt.xlabel('Time t')

plt.ylabel('M(t)')

plt.grid(True)

plt.legend()

plt.show()

import numpy as np

import matplotlib.pyplot as plt

def simulate_gbm(S0, mu, sigma, T, N, num_paths):

dt = T / N

t = np.linspace(0, T, N)

paths = []

for _ in range(num_paths):

W = np.random.normal(0, np.sqrt(dt), N)

W = np.cumsum(W) # cumulative sum to represent Brownian motion

S = S0 * np.exp((mu - 0.5 * sigma**2) * t + sigma * W)

paths.append(S)

return t, paths

# Parameters

S0 = 100 # Initial value of the asset

mu = 0.05 # Drift

sigma = 0.2 # Volatility

T = 1 # Time horizon (1 year)

N = 1000 # Number of time steps

num_paths = 5 # Number of paths to simulate

t, paths = simulate_gbm(S0, mu, sigma, T, N, num_paths)

# Plotting the simulated GBM paths

plt.figure(figsize=(10, 6))

for i, S in enumerate(paths):

plt.plot(t, S, label=f'Path {i + 1}')

plt.xlabel('Time')

plt.ylabel('Price')

plt.title('Sampled paths from Geometric Brownian Motion')

plt.grid(True)

plt.show()

Simulation using Gaussian Processes¶

import GPy

import numpy as np

import matplotlib.pyplot as plt

# Parameters for Geometric Brownian Motion

S0 = 100 # Initial value of the asset

mu = 0.05 # Drift

sigma = 0.2 # Volatility

T = 1 # Time horizon (1 year)

n = 1000 # Number of steps

t = np.linspace(0, T, n+1).reshape(-1, 1) # Time points

# Define the custom kernel for Brownian motion

class GBMKernel(GPy.kern.Kern):

def __init__(self, input_dim, sigma=1.0, active_dims=None):

super(GBMKernel, self).__init__(input_dim, active_dims, 'Brownian')

self.sigma = GPy.core.Param('sigma', sigma)

self.link_parameters(self.sigma)

def K(self, X, X2=None):

if X2 is None:

X2 = X

t1 = X

t2 = X2.T

# Covariance function of Brownian motion: sigma^2 * min(s, t)

cov_matrix = self.sigma**2 * np.minimum(t1, t2)

return cov_matrix

def Kdiag(self, X):

return self.sigma**2 * X[:, 0]

# No-op for gradient update since we are not optimizing the kernel

def update_gradients_full(self, dL_dK, X, X2=None):

pass

# No-op for kernel gradient since we are not optimizing the kernel

def gradients_X(self, dL_dK, X, X2=None):

return np.zeros(X.shape)

# Custom mean function to include drift

class GBMMean(GPy.core.Mapping):

def __init__(self, input_dim, output_dim, S0=0.0, mu=0.0):

super(GBMMean, self).__init__(input_dim, output_dim)

self.S0 = S0 # Initial value

self.mu = mu # Drift coefficient

def f(self, X):

# Mean function: S0 + mu * t

return self.S0 + self.mu * X

def update_gradients(self, dL_df, X):

pass

def gradients_X(self, dL_df, X):

return np.zeros(X.shape)

# Instantiate the Brownian motion kernel with parameters

bm_kernel = GBMKernel(input_dim=1, sigma=sigma)

# Instantiate the mean function with S0 and mu

mean_function = GBMMean(input_dim=1, output_dim=1, S0=np.log(S0), mu=mu)

# Provide the initial observation at t=0

t_data = np.array([[0.0]])

Y_data = np.array([[np.log(S0)]])

# Create a GP model with the custom mean function and Brownian motion kernel

model = GPy.models.GPRegression(t_data, Y_data, kernel=bm_kernel, mean_function=mean_function)

# Set noise variance to a negligible value since we're simulating without observation noise

model.likelihood.variance.fix(1e-10)

# Sample paths from the GP model

num_samples = 5

samples = model.posterior_samples_f(t, size=num_samples)

# Transform samples to original GBM scale

gbm_samples = np.exp(samples)

# Plot the sampled paths

plt.figure(figsize=(10, 6))

for i in range(num_samples):

plt.plot(t, gbm_samples[:, :, i], label=f'Path {i+1}')

plt.title(f'Sampled Paths from Geometric Brownian Motion')

plt.xlabel('Time t')

plt.ylabel('S(t)')

plt.grid(True)

plt.legend()

plt.show()

Orstein - Uhlenbeck process¶

Simulation using discrete paths¶

import numpy as np

import matplotlib.pyplot as plt

# Parameters for the Ornstein-Uhlenbeck process

S0 = 5.0 # Initial value

mu = 1.0 # Long-term mean

theta = 10 # Rate of mean reversion

sigma = 1 # Volatility

T = 1.0 # Total time

n = 100 # Number of steps

dt = T / n # Time step size

t = np.linspace(0, T, n+1) # Time points

# Number of paths to simulate

num_paths = 5

# Set up the plot

plt.figure(figsize=(10, 6))

# Simulate multiple paths

for _ in range(num_paths):

S = np.zeros(n+1) # Initialize the process

S[0] = S0 # Set initial value

for i in range(1, n+1):

# Compute the mean and variance for the next step

mean = S0 * np.exp(-theta * t[i]) + mu * (1 - np.exp(-theta * t[i]))

variance = (sigma**2 / (2 * theta)) * (1 - np.exp(-2 * theta * t[i]))

# Sample from the normal distribution with the computed mean and variance

S[i] = np.random.normal(mean, np.sqrt(variance))

# Plot the Ornstein-Uhlenbeck path

plt.plot(t, S, label=f'Path {_+1}')

# Customize the plot

plt.title('Sampled Paths from the Ornstein-Uhlenbeck Process')

plt.xlabel('Time t')

plt.ylabel('S(t)')

plt.grid(True)

plt.legend()

plt.show()

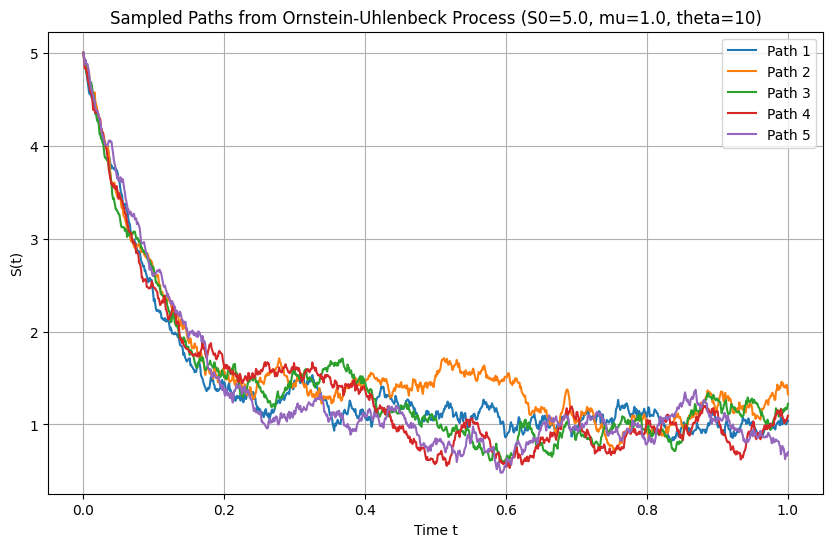

Simulation using Gaussian Processes¶

import GPy

import numpy as np

import matplotlib.pyplot as plt

# Parameters for the Ornstein-Uhlenbeck process

S0 = 5.0 # Initial value

mu = 1.0 # Long-term mean

theta = 10 # Rate of mean reversion

sigma = 1 # Volatility

T = 1.0 # Total time

n = 1000 # Number of steps

t = np.linspace(0, T, n+1).reshape(-1, 1) # Time points

# Define the custom kernel for the Ornstein-Uhlenbeck process

class OrnsteinUhlenbeckKernel(GPy.kern.Kern):

def __init__(self, input_dim, theta=1.0, sigma=1.0, active_dims=None):

super(OrnsteinUhlenbeckKernel, self).__init__(input_dim, active_dims, 'OU')

self.theta = GPy.core.Param('theta', theta)

self.sigma = GPy.core.Param('sigma', sigma)

self.link_parameters(self.theta, self.sigma)

def K(self, X, X2=None):

if X2 is None:

X2 = X

t1 = X

t2 = X2.T

min_t = np.minimum(t1, t2)

# Covariance function of the Ornstein-Uhlenbeck process

cov_matrix = (self.sigma**2 / (2 * self.theta)) * np.exp(-self.theta * np.abs(t1 - t2)) * (1 - np.exp(-2 * self.theta * min_t))

return cov_matrix

def Kdiag(self, X):

return (self.sigma**2 / (2 * self.theta)) * (1 - np.exp(-2 * self.theta * X[:, 0]))

# No-op for gradient update since we are not optimizing the kernel

def update_gradients_full(self, dL_dK, X, X2=None):

pass

# No-op for kernel gradient since we are not optimizing the kernel

def gradients_X(self, dL_dK, X, X2=None):

return np.zeros(X.shape)

# Custom mean function to include mean-reverting drift toward mu

class OUProcessMean(GPy.core.Mapping):

def __init__(self, input_dim, output_dim, S0=0.0, mu=0.0, theta=1.0):

super(OUProcessMean, self).__init__(input_dim, output_dim)

self.S0 = S0 # Initial value

self.mu = mu # Long-term mean

self.theta = theta # Rate of mean reversion

def f(self, X):

# Mean function: S_0 * exp(-theta * t) + mu * (1 - exp(-theta * t))

return self.S0 * np.exp(-self.theta * X) + self.mu * (1 - np.exp(-self.theta * X))

def update_gradients(self, dL_df, X):

pass

def gradients_X(self, dL_df, X):

return np.zeros(X.shape)

# Instantiate the OU kernel with parameters

ou_kernel = OrnsteinUhlenbeckKernel(input_dim=1, theta=theta, sigma=sigma)

# Instantiate the mean function with non-zero initial value S0 and long-term mean mu

mean_function = OUProcessMean(input_dim=1, output_dim=1, S0=S0, mu=mu, theta=theta)

# Provide the initial observation at t=0

t_data = np.array([[0.0]])

Y_data = np.array([[S0]])

# Create a GP model with the custom mean function and OU kernel

model = GPy.models.GPRegression(t_data, Y_data, kernel=ou_kernel, mean_function=mean_function)

# Set noise variance to a negligible value since we're simulating without observation noise

model.likelihood.variance.fix(1e-10)

# Sample paths from the GP model

num_samples = 5

samples = model.posterior_samples_f(t, size=num_samples)

# Plot the sampled paths

plt.figure(figsize=(10, 6))

for i in range(num_samples):

plt.plot(t, samples[:, :, i], label=f'Path {i+1}')

plt.title(f'Sampled Paths from Ornstein-Uhlenbeck Process (S0={S0}, mu={mu}, theta={theta})')

plt.xlabel('Time t')

plt.ylabel('S(t)')

plt.grid(True)

plt.legend()

plt.show()

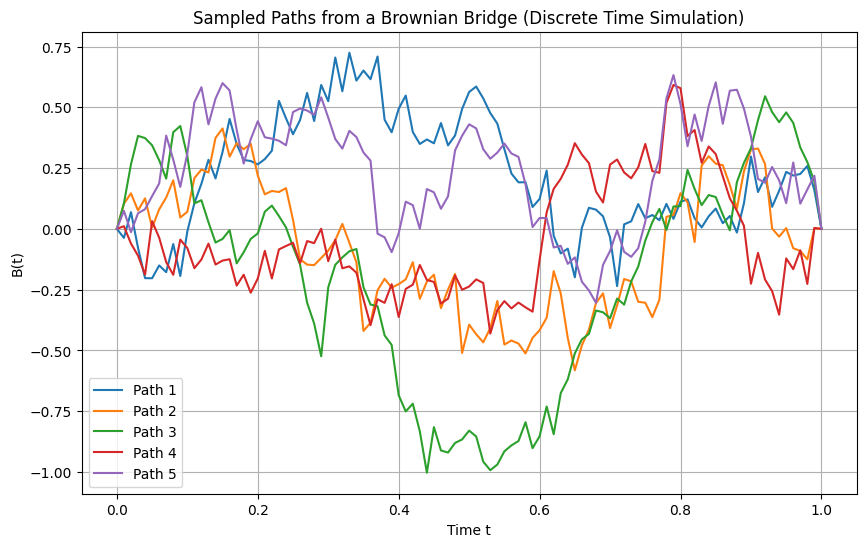

import numpy as np

import matplotlib.pyplot as plt

# Parameters for the Brownian bridge

T = 1.0 # Total time

n = 100 # Number of steps

dt = T / n # Time step size

t = np.linspace(0, T, n+1) # Time points

# Number of paths to simulate

num_paths = 5

# Set up the plot

plt.figure(figsize=(10, 6))

# Simulate multiple paths

for _ in range(num_paths):

W = np.zeros(n+1) # Initialize the Wiener process

for i in range(1, n+1):

W[i] = W[i-1] + np.sqrt(dt) * np.random.randn() # Standard Wiener process

# Adjust Wiener process to form a Brownian bridge

B = W - (t / T) * W[-1] # Brownian bridge: W(t) - (t/T) * W(T)

# Plot the Brownian bridge path

plt.plot(t, B, label=f'Path {_+1}')

# Customize the plot

plt.title('Sampled Paths from a Brownian Bridge (Discrete Time Simulation)')

plt.xlabel('Time t')

plt.ylabel('B(t)')

plt.grid(True)

plt.legend()

plt.show()

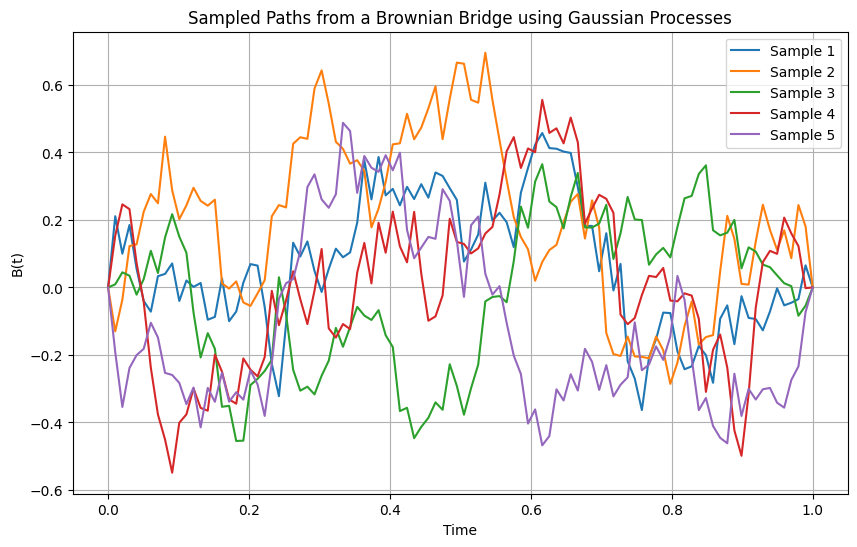

Simulation using Gaussian processes¶

import GPy

import numpy as np

import matplotlib.pyplot as plt

# Time points at which to sample the Brownian bridge

T = 1.0

t = np.linspace(0, T, 100).reshape(-1, 1)

# Define a custom kernel for the Brownian bridge

class BrownianBridgeKernel(GPy.kern.Kern):

def __init__(self, input_dim, variance=1.0, active_dims=None):

super(BrownianBridgeKernel, self).__init__(input_dim, active_dims, 'brownian_bridge')

self.variance = GPy.core.Param('variance', variance)

self.link_parameter(self.variance)

def K(self, X, X2=None):

if X2 is None:

X2 = X

t1 = X

t2 = X2.T

T = np.max(X)

# Brownian bridge kernel: min(t1, t2) - (t1 * t2) / T

cov_matrix = np.minimum(t1, t2) - (t1 * t2) / T

return self.variance * cov_matrix

def Kdiag(self, X):

return self.variance * (X[:, 0] - (X[:, 0]**2) / T)

# No-op for gradient update since we are not optimizing the kernel

def update_gradients_full(self, dL_dK, X, X2=None):

pass

# No-op for kernel gradient since we are not optimizing the kernel

def gradients_X(self, dL_dK, X, X2=None):

return np.zeros(X.shape)

# Instantiate the Brownian bridge kernel with variance 1

brownian_bridge_kernel = BrownianBridgeKernel(input_dim=1, variance=1.0)

# Create a GP model with zero mean function

mean_function = GPy.mappings.Constant(input_dim=1, output_dim=1, value=0)

model = GPy.models.GPRegression(t, np.zeros_like(t), kernel=brownian_bridge_kernel, mean_function=mean_function)

# Sample paths from the GP model without optimizing (since Brownian bridge doesn't require fitting)

num_samples = 5

samples = model.posterior_samples_f(t, size=num_samples)

# Plot the sampled paths

plt.figure(figsize=(10, 6))

for i in range(num_samples):

plt.plot(t, samples[:, :, i], label=f'Sample {i+1}')

plt.title('Sampled Paths from a Brownian Bridge using Gaussian Processes')

plt.xlabel('Time')

plt.ylabel('B(t)')

plt.grid(True)

plt.legend()

plt.show()

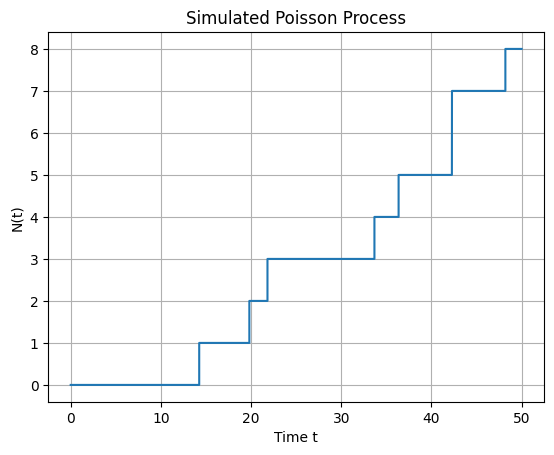

import numpy as np

import matplotlib.pyplot as plt

# Parameters

lambda_rate = 0.2 # The rate parameter λ of the Poisson process

T = 50 # Total time

delta_t = 0.01 # Time-step Δt

num_steps = int(T / delta_t) # Number of time steps

# Time grid

t = np.linspace(0, T, num_steps + 1)

# Initialize N_t

N_t = np.zeros(num_steps + 1, dtype=int)

# Simulate the Poisson process

for i in range(1, num_steps + 1):

# Generate a random number between 0 and 1

u = np.random.rand()

# If u < λΔt, increment N_t

if u < lambda_rate * delta_t:

N_t[i] = N_t[i - 1] + 1

else:

N_t[i] = N_t[i - 1]

# Plot the Poisson process

plt.step(t, N_t, where='post')

plt.xlabel('Time t')

plt.ylabel('N(t)')

plt.title('Simulated Poisson Process')

plt.grid(True)

plt.show()

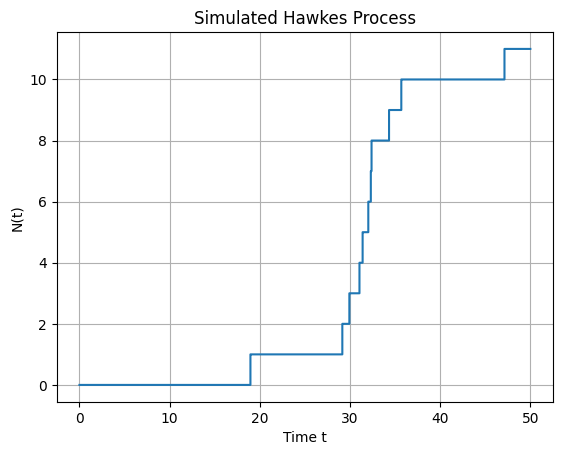

Hawkes process¶

import numpy as np

import matplotlib.pyplot as plt

# Parameters

mu = 0.2 # Baseline intensity (μ)

alpha = 0.5 # Excitation parameter (α)

beta = 1 # Decay rate (β)

T = 50 # Total time to simulate

delta_t = 0.01 # Time-step Δt

# Time grid

time_grid = np.arange(0, T + delta_t, delta_t)

num_steps = len(time_grid)

# Initialize N_t and event times

N_t = np.zeros(num_steps, dtype=int)

event_times = []

# Simulate the Hawkes process

for i in range(1, num_steps):

t_i = time_grid[i]

# Compute lambda_t

lambda_t = mu

if event_times:

tau_array = np.array(event_times)

lambda_t += np.sum(alpha * np.exp(-beta * (t_i - tau_array)))

# Calculate the event probability

p = lambda_t * delta_t

if p > 1.0:

p = 1.0 # Ensure probability does not exceed 1

# Simulate event occurrence

u = np.random.rand()

if u < p:

N_t[i] = N_t[i - 1] + 1

event_times.append(t_i)

else:

N_t[i] = N_t[i - 1]

# Plot the counting process

#plt.figure(figsize=(12, 6))

plt.step(time_grid, N_t, where='post')

plt.xlabel('Time t')

plt.ylabel('N(t)')

plt.title('Simulated Hawkes Process')

plt.grid(True)

plt.show()

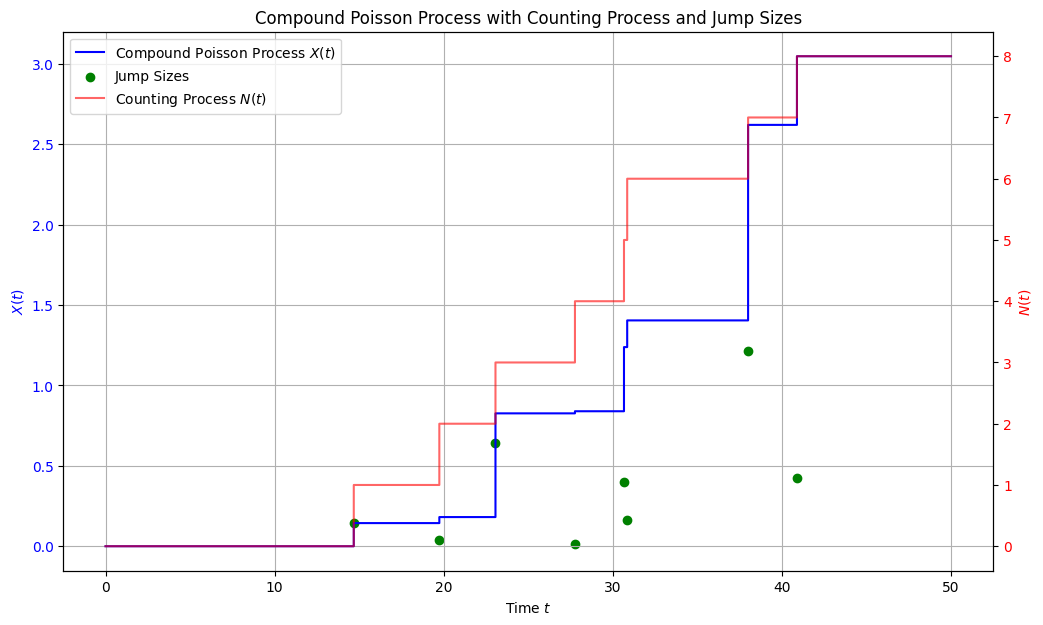

Compound Poisson process¶

import numpy as np

import matplotlib.pyplot as plt

# Parameters

lambda_rate = 0.2 # Rate parameter λ of the Poisson process

T = 50 # Total simulation time

delta_t = 0.01 # Time-step Δt

num_steps = int(T / delta_t)

time_grid = np.linspace(0, T, num_steps + 1)

# Jump size distribution parameters

eta = 2.5 # Rate parameter of the exponential distribution for jump sizes

# Initialize arrays

N_t = np.zeros(num_steps + 1, dtype=int) # Counting process N(t)

X_t = np.zeros(num_steps + 1) # Compound Poisson process X(t)

event_times = [] # Times when events occur

jump_sizes = [] # Sizes of the jumps

# Simulate the compound Poisson process

for i in range(1, num_steps + 1):

t = time_grid[i]

# Probability of an event in [t_i, t_i + delta_t)

p = lambda_rate * delta_t

# Ensure probability does not exceed 1

p = min(p, 1.0)

# Determine if an event occurs

if np.random.rand() < p:

N_t[i] = N_t[i - 1] + 1

# Sample a jump size Y_i from an exponential distribution

Y_i = np.random.exponential(scale=1/eta)

jump_sizes.append(Y_i)

event_times.append(t)

X_t[i] = X_t[i - 1] + Y_i

else:

N_t[i] = N_t[i - 1]

X_t[i] = X_t[i - 1]

# Plot all three visualizations in one figure

fig, ax1 = plt.subplots(figsize=(12, 7))

# Plot the compound Poisson process X(t)

ax1.step(time_grid, X_t, where='post', label='Compound Poisson Process $X(t)$', color='blue')

ax1.set_xlabel('Time $t$')

ax1.set_ylabel('$X(t)$', color='blue')

ax1.tick_params(axis='y', labelcolor='blue')

ax1.grid(True)

# Plot jump sizes as scatter points on X(t)

event_indices = [np.searchsorted(time_grid, t) for t in event_times]

event_values = [X_t[idx] for idx in event_indices]

ax1.scatter(event_times, jump_sizes, color='green', marker='o', label='Jump Sizes')

# Create a secondary y-axis for the counting process N(t)

ax2 = ax1.twinx()

ax2.step(time_grid, N_t, where='post', label='Counting Process $N(t)$', color='red', alpha=0.6)

ax2.set_ylabel('$N(t)$', color='red')

ax2.tick_params(axis='y', labelcolor='red')

# Combine legends from both axes

lines1, labels1 = ax1.get_legend_handles_labels()

lines2, labels2 = ax2.get_legend_handles_labels()

ax1.legend(lines1 + lines2, labels1 + labels2, loc='upper left')

plt.title('Compound Poisson Process with Counting Process and Jump Sizes')

plt.show()

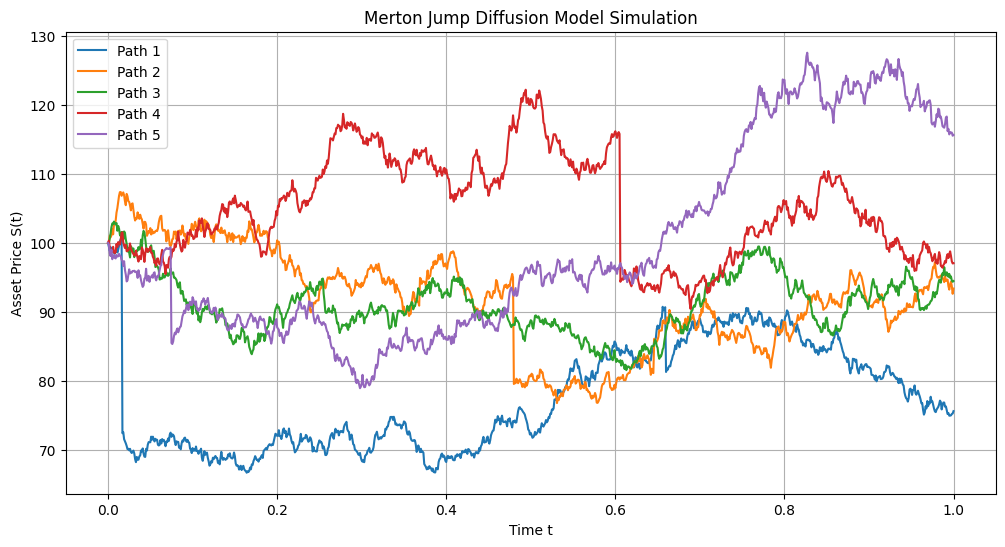

Jump diffusion processes¶

import numpy as np

import matplotlib.pyplot as plt

def simulate_merton_jump_diffusion(S0, mu, sigma, lamb, mu_j, sigma_j, T, N, M):

"""

Simulate the Merton jump diffusion model.

Parameters:

- S0: Initial asset price.

- mu: Expected return (drift rate).

- sigma: Volatility of the continuous component.

- lamb: Jump intensity (average number of jumps per unit time).

- mu_j: Mean of the jump size distribution (of ln(J)).

- sigma_j: Standard deviation of the jump size distribution (of ln(J)).

- T: Total time horizon.

- N: Number of time steps.

- M: Number of simulation paths.

Returns:

- t: Array of time points.

- S: Matrix of simulated asset prices (M paths x N+1 time points).

"""

dt = T / N # Time step size

t = np.linspace(0, T, N + 1) # Time grid

# Precompute constants

drift = (mu - 0.5 * sigma**2) * dt

diffusion = sigma * np.sqrt(dt)

# Initialize asset price paths

S = np.zeros((M, N + 1))

S[:, 0] = S0

for m in range(M):

# Initialize variables for each path

S_m = np.zeros(N + 1)

S_m[0] = S0

# Generate random numbers for Brownian motion

Z = np.random.normal(size=N)

# Generate random numbers for jumps

# Poisson random numbers for number of jumps in each time step

Nt = np.random.poisson(lamb * dt, size=N)

# Total number of jumps

num_jumps = np.sum(Nt)

# Generate jump sizes only where jumps occur

if num_jumps > 0:

jump_sizes = np.random.normal(loc=mu_j, scale=sigma_j, size=num_jumps)

else:

jump_sizes = np.array([])

# Index to keep track of jump sizes

jump_index = 0

for i in range(1, N + 1):

# Continuous part

S_m[i] = S_m[i - 1] * np.exp(drift + diffusion * Z[i - 1])

# Jump part

if Nt[i - 1] > 0:

# Apply jumps

total_jump = np.sum(jump_sizes[jump_index:jump_index + Nt[i - 1]])

S_m[i] *= np.exp(total_jump)

jump_index += Nt[i - 1]

S[m, :] = S_m

return t, S

# Parameters

S0 = 100 # Initial asset price

mu = 0.1 # Expected return

sigma = 0.2 # Volatility

lamb = 1 # Jump intensity λ

k = -0.1 # Mean of ln(J) (jump sizes)

delta = 0.1 # Std dev of ln(J)

T = 1.0 # Total time (e.g., 1 year)

N = 1000 # Number of time steps

M = 5 # Number of simulation paths

# Simulate the Merton jump diffusion model

t, S = simulate_merton_jump_diffusion(S0, mu, sigma, lamb, k, delta, T, N, M)

# Plot the simulated asset price paths

plt.figure(figsize=(12, 6))

for m in range(M):

plt.plot(t, S[m, :], label=f'Path {m + 1}')

plt.xlabel('Time t')

plt.ylabel('Asset Price S(t)')

plt.title('Merton Jump Diffusion Model Simulation')

plt.legend()

plt.grid(True)

plt.show()