Bayesian Modelling#

Bayesian probability#

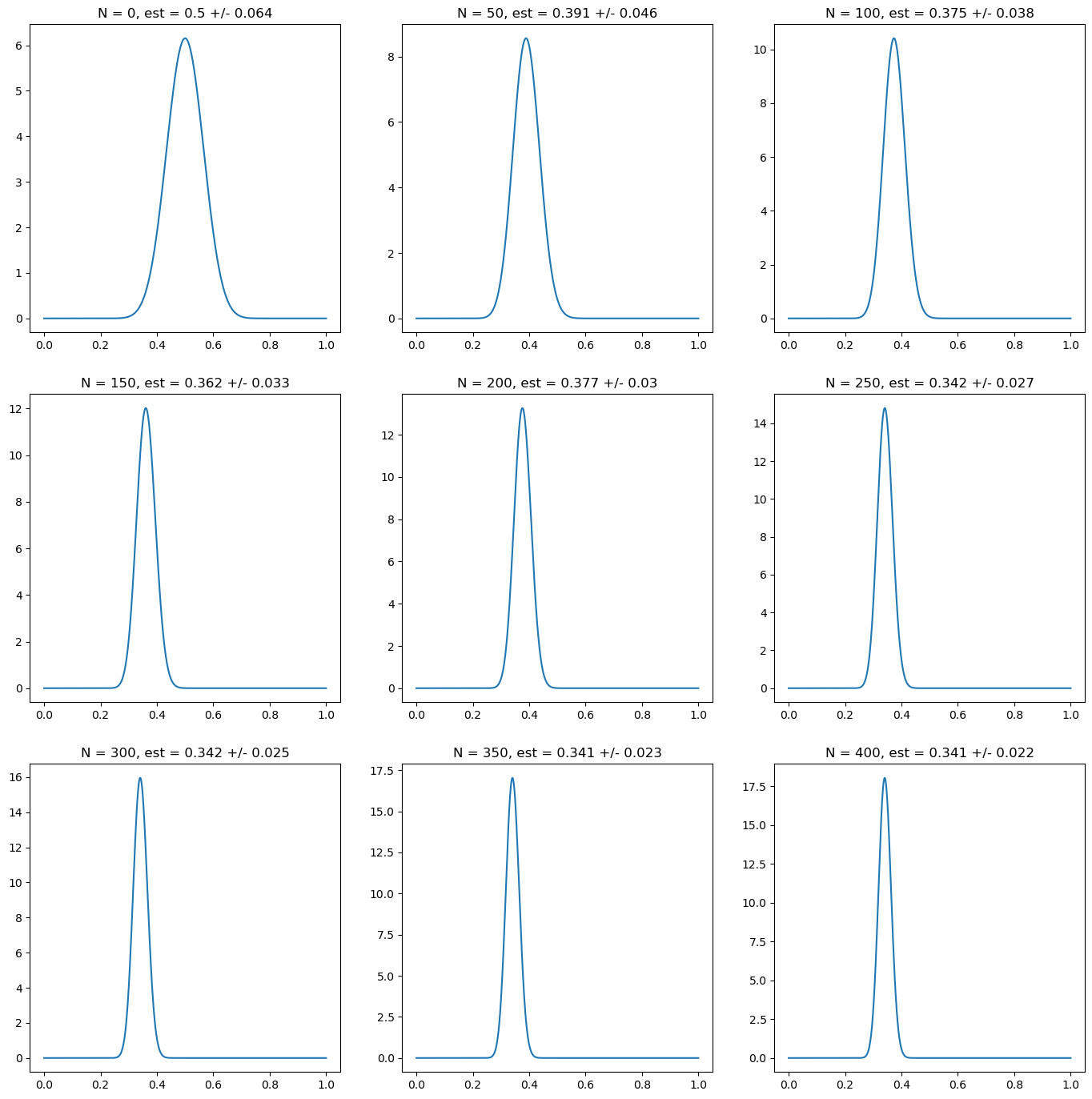

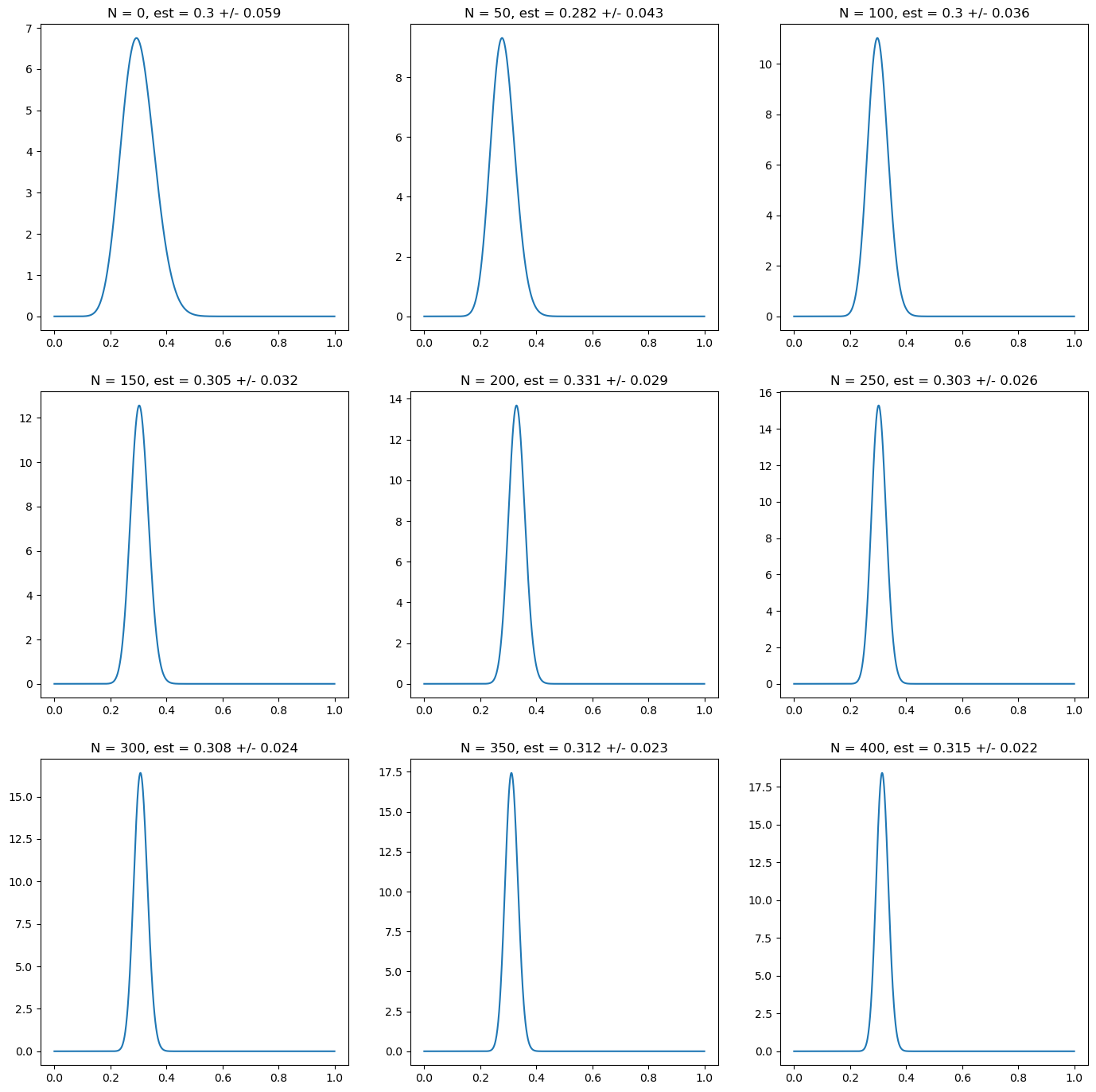

Example: estimating the probability of heads in a coin toss experiment#

# Generate a sequence of binary random variables

from scipy.stats import bernoulli, beta, uniform

p = 0.3

r = bernoulli.rvs(p, size=400)

r[:10]

array([0, 0, 0, 1, 0, 0, 0, 1, 0, 0])

import matplotlib.pyplot as plt

import numpy as np

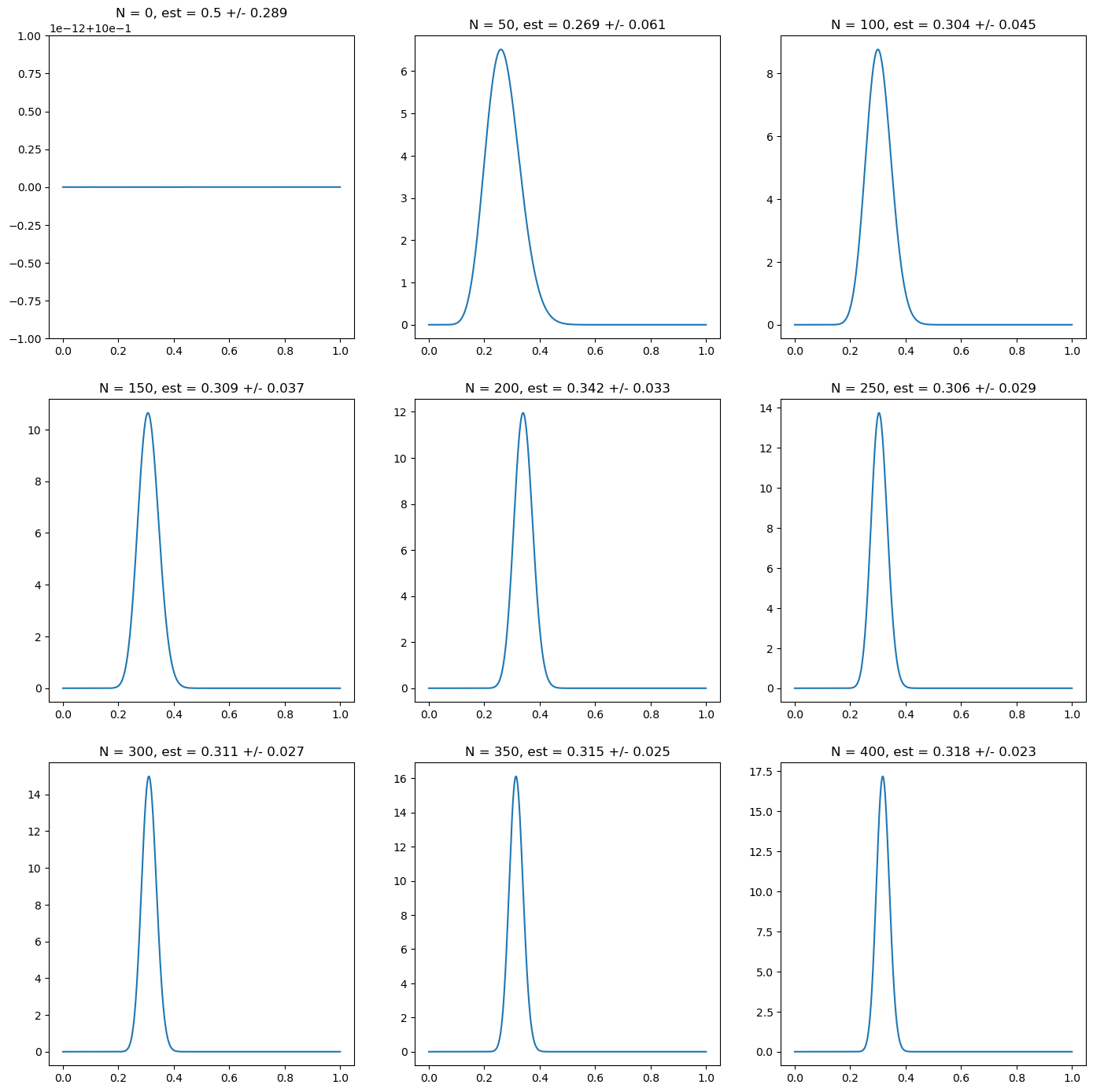

# prior distribution: uniform prior

prior_alpha = 1

prior_beta = 1

# Now we plot the distribution as we add more data points

fig, ax = plt.subplots(nrows=3, ncols=3, figsize=(17,17))

N = np.linspace(0, len(r), 9)

for i in range(9):

n = N[i]

i_x = int(i/3)

i_y = i % 3

r_trunc = r[:int(n)]

p_grid = np.linspace(0, 1, 1000)

post_alpha = prior_alpha + np.sum(r_trunc)

post_beta = prior_beta + len(r_trunc)- np.sum(r_trunc)

mean = beta.mean(post_alpha, post_beta)

std = beta.std(post_alpha, post_beta)

ax[i_x][i_y].plot(p_grid, beta.pdf(p_grid, post_alpha, post_beta))

ax[i_x][i_y].set_title("N = " + str(int(n))+ ", est = " + str(np.round(mean, 3)) + " +/- " + str(np.round(std, 3)))

import matplotlib.pyplot as plt

import numpy as np

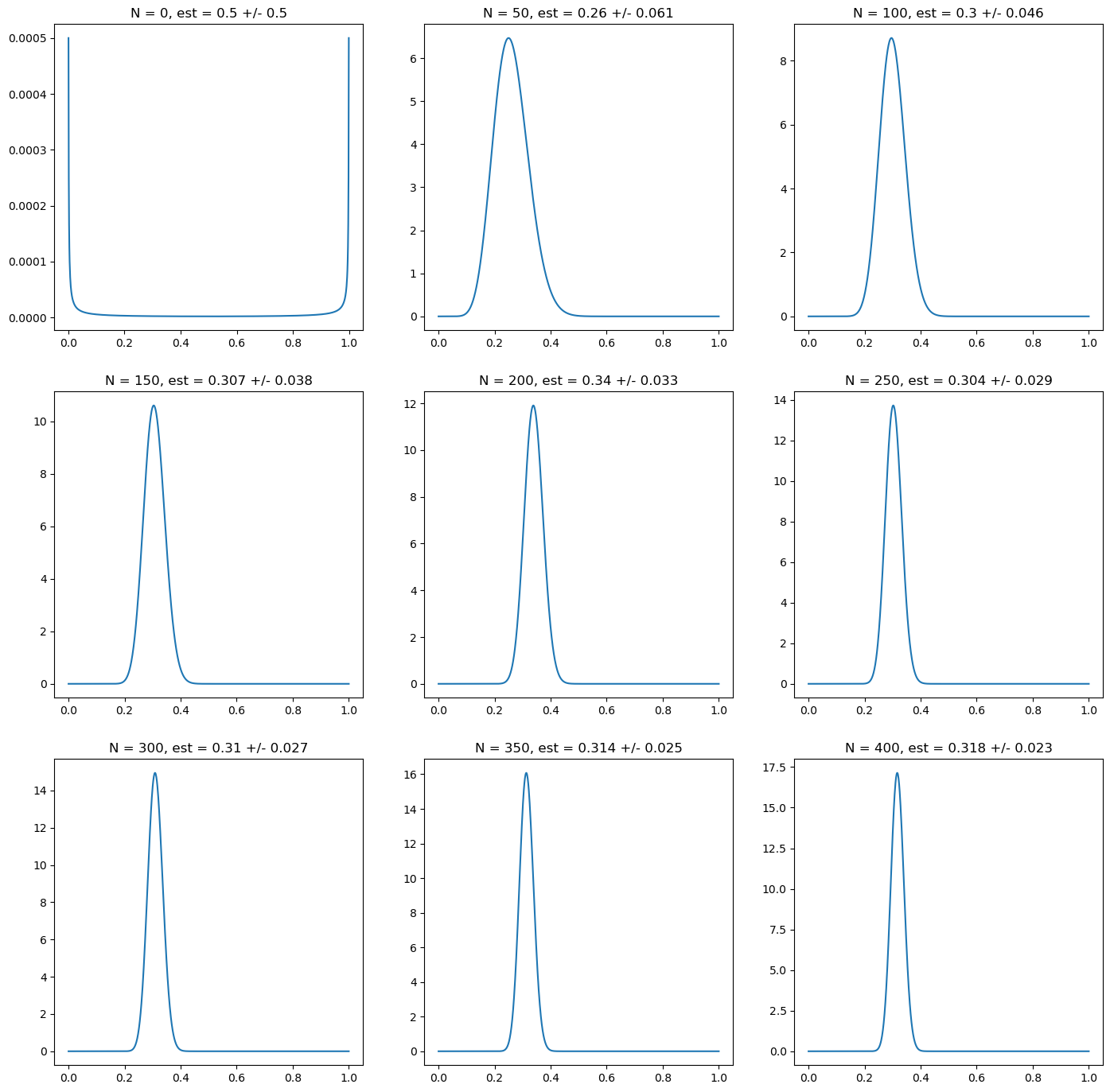

# prior distribution: non - informative prior (approximation)

prior_alpha = 0.000001

prior_beta = 0.000001

# Now we plot the distribution as we add more data points

fig, ax = plt.subplots(nrows=3, ncols=3, figsize=(17,17))

N = np.linspace(0, len(r), 9)

for i in range(9):

n = N[i]

i_x = int(i/3)

i_y = i % 3

r_trunc = r[:int(n)]

post_alpha = prior_alpha + np.sum(r_trunc)

post_beta = prior_beta + len(r_trunc)- np.sum(r_trunc)

mean = beta.mean(post_alpha, post_beta)

std = beta.std(post_alpha, post_beta)

ax[i_x][i_y].plot(p_grid, beta.pdf(p_grid, post_alpha, post_beta))

ax[i_x][i_y].set_title("N = " + str(int(n))+ ", est = " + str(np.round(mean, 3)) + " +/- " + str(np.round(std, 3)))

import matplotlib.pyplot as plt

import numpy as np

# prior distribution: wrong confident prior

prior_alpha = 30

prior_beta = 30

# Now we plot the distribution as we add more data points

fig, ax = plt.subplots(nrows=3, ncols=3, figsize=(17,17))

N = np.linspace(0, len(r), 9)

for i in range(9):

n = N[i]

i_x = int(i/3)

i_y = i % 3

r_trunc = r[:int(n)]

post_alpha = prior_alpha + np.sum(r_trunc)

post_beta = prior_beta + len(r_trunc)- np.sum(r_trunc)

mean = beta.mean(post_alpha, post_beta)

std = beta.std(post_alpha, post_beta)

ax[i_x][i_y].plot(p_grid, beta.pdf(p_grid, post_alpha, post_beta))

ax[i_x][i_y].set_title("N = " + str(int(n))+ ", est = " + str(np.round(mean, 3)) + " +/- " + str(np.round(std, 3)))

import matplotlib.pyplot as plt

import numpy as np

# prior distribution: correct confident prior

prior_alpha = 18

prior_beta = 42

# Now we plot the distribution as we add more data points

fig, ax = plt.subplots(nrows=3, ncols=3, figsize=(17,17))

N = np.linspace(0, len(r), 9)

for i in range(9):

n = N[i]

i_x = int(i/3)

i_y = i % 3

r_trunc = r[:int(n)]

post_alpha = prior_alpha + np.sum(r_trunc)

post_beta = prior_beta + len(r_trunc)- np.sum(r_trunc)

mean = beta.mean(post_alpha, post_beta)

std = beta.std(post_alpha, post_beta)

ax[i_x][i_y].plot(p_grid, beta.pdf(p_grid, post_alpha, post_beta))

ax[i_x][i_y].set_title("N = " + str(int(n))+ ", est = " + str(np.round(mean, 3)) + " +/- " + str(np.round(std, 3)))

Estimation of Latent Variable Models#

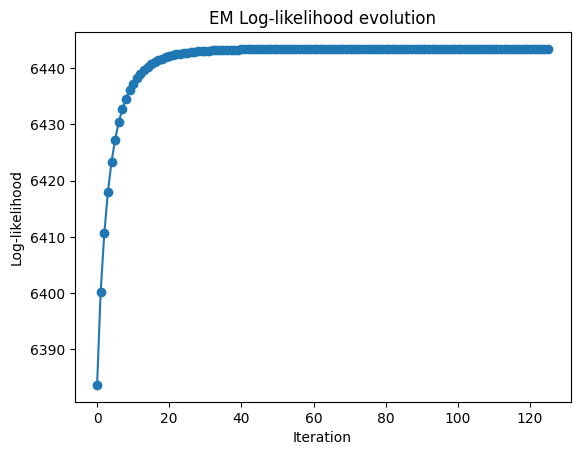

Expectation Maximization#

Example 1: Gaussian Mixture Models#

from scipy.stats import norm

import numpy as np

class TheGoodAndBadDataModel():

def __init__(self, prior_p_good, prior_mean, prior_std_good, prior_std_bad):

self.p_good = prior_p_good

self.mean = prior_mean

self.std_good = prior_std_good

self.std_bad = prior_std_bad

self.loglik_history = [] # store likelihood values

def predict(self, X):

p_x_bad_pbad = (1 - self.p_good) * norm.pdf(X, loc=self.mean, scale=self.std_bad)

p_x_good_pgood = self.p_good * norm.pdf(X, loc=self.mean, scale=self.std_good)

p_bad_x = p_x_bad_pbad / (p_x_good_pgood + p_x_bad_pbad)

return p_bad_x

def compute_loglik(self, X):

mixture_pdf = (

self.p_good * norm.pdf(X, loc=self.mean, scale=self.std_good) +

(1 - self.p_good) * norm.pdf(X, loc=self.mean, scale=self.std_bad)

)

return np.sum(np.log(mixture_pdf + 1e-12)) # add epsilon to avoid log(0)

def learn(self, X, max_iter=1000, tolerance=1e-5, print_error=False, track_likelihood=True):

iter = 0

while True:

iter += 1

# E-step

p_bad_s = self.predict(X)

p_good_s = 1 - p_bad_s

# M-step

p_good_sp1 = np.mean(p_good_s)

std_good_sp1 = np.sqrt(np.sum(p_good_s * (X - self.mean)**2) / (len(X) * p_good_sp1))

std_bad_sp1 = np.sqrt(np.sum(p_bad_s * (X - self.mean)**2) / (len(X) * (1 - p_good_sp1)))

# compute change (for stopping)

error = np.sqrt(((p_good_sp1 - self.p_good)/self.p_good)**2

+ ((std_good_sp1 - self.std_good)/self.std_good)**2

+ ((std_bad_sp1 - self.std_bad)/self.std_bad)**2)

# update parameters

self.p_good = p_good_sp1

self.std_good = std_good_sp1

self.std_bad = std_bad_sp1

# track log-likelihood

if track_likelihood:

ll = self.compute_loglik(X)

self.loglik_history.append(ll)

if print_error:

print(f"Iter {iter}: error={error:.6f}, loglik={ll:.6f}")

# stopping condition

if (error < tolerance or iter >= max_iter):

break

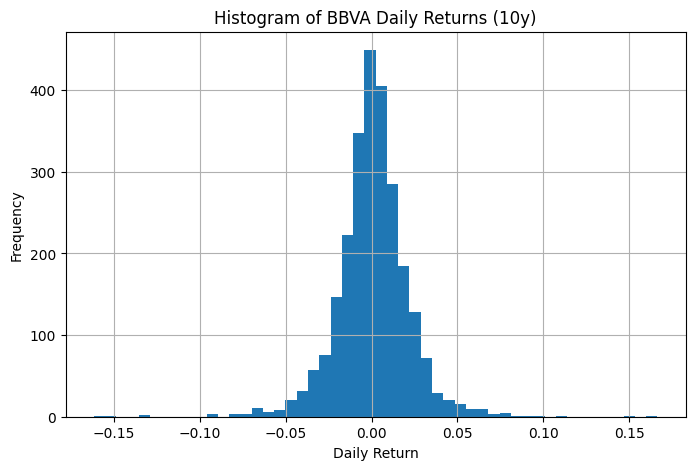

import yfinance as yf

import numpy as np

# Define ticker

bbva_tkr = yf.Ticker("BBVA.MC")

# Get 10 years of daily adjusted close prices

end_date = "2025-07-31"

start_date = "2015-07-31" # 10 years earlier

data = bbva_tkr.history(start=start_date, end=end_date, interval="1d")["Close"]

data = bbva_tkr.history(period="10y", interval="1d")["Close"]

# Calculate daily returns

bbva_ret = data.pct_change().dropna()

# Print mean and standard deviation of returns

print("Mean return:", np.mean(bbva_ret))

print("Std deviation:", np.std(bbva_ret))

Mean return: 0.0006867420397232735

Std deviation: 0.021392342218226022

# We learn the model over the historical data. As a prior we assume there are only 10% anomalies in the dataset

# The result is relatively robust to the choice of prior

gbdm = TheGoodAndBadDataModel(0.99, np.mean(bbva_ret), np.std(bbva_ret), 2*np.std(bbva_ret))

gbdm.learn(bbva_ret)

# We have a look at the results: according to the model, there are 15% anomalies, with roughly a 3x standard deviation

# This means the model detects that the distribution of returns is not accurately described by a single Gaussian

print(gbdm.p_good, gbdm.mean, gbdm.std_good, gbdm.std_bad)

0.8494092741093464 0.0006867420397232735 0.01482171389384633 0.04242390635242809

# Plot the log-likelihood history

import matplotlib.pyplot as plt

plt.plot(gbdm.loglik_history, marker="o")

plt.xlabel("Iteration")

plt.ylabel("Log-likelihood")

plt.title("EM Log-likelihood evolution")

plt.show()

import matplotlib.pyplot as plt

bbva_ret.hist(bins=50, figsize=(8,5))

plt.xlabel("Daily Return")

plt.ylabel("Frequency")

plt.title("Histogram of BBVA Daily Returns (10y)")

plt.show()

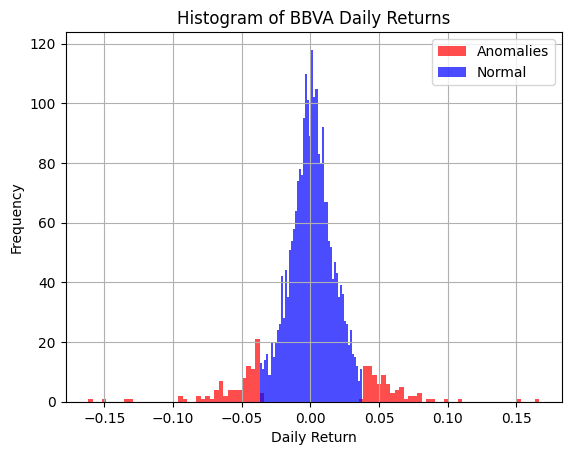

# Let us flag anomalies as those with 50% of more probability of belonging to the "bad data" mixture component

anomalies = (gbdm.predict(bbva_ret) > 0.5)

# Add anomaly flag to DataFrame

pd_bbva_ret = bbva_ret.reset_index()

pd_bbva_ret.columns = ["Date", "Returns"]

pd_bbva_ret["anomaly"] = anomalies

# Plot histogram of returns, segmented by anomaly flag

pd_bbva_ret[pd_bbva_ret["anomaly"] == True]["Returns"].hist(

bins=100, alpha=0.7, color="red", label="Anomalies")

pd_bbva_ret[pd_bbva_ret["anomaly"] == False]["Returns"].hist(

bins=50, alpha=0.7, color="blue", label="Normal")

plt.xlabel("Daily Return")

plt.ylabel("Frequency")

plt.title("Histogram of BBVA Daily Returns")

plt.legend()

plt.show()

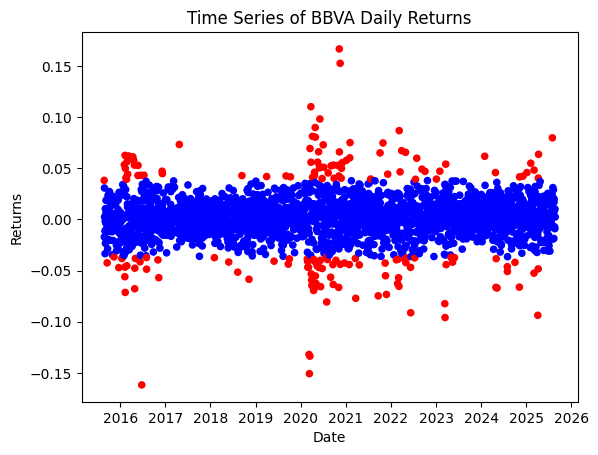

# In terms of time-series, we flat the anomalies in the following plot

colors = {False: "blue", True: "red"}

pd_bbva_ret.reset_index().plot.scatter(x = "Date", y = "Returns", c = pd_bbva_ret["anomaly"].map(colors).values, title = "Time Series of BBVA Daily Returns")

<Axes: title={'center': 'Time Series of BBVA Daily Returns'}, xlabel='Date', ylabel='Returns'>

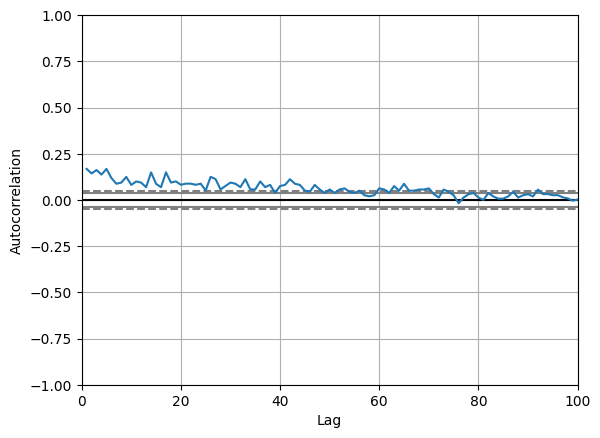

# An interesting question is whether these anomalies tend to cluster. Looking at the auto-correlation it hints this is a possibility

# This means it could make sense to analyse these anomalies as regime changes, i.e. use a hidden markov model

from pandas.plotting import autocorrelation_plot

ax = autocorrelation_plot(pd_bbva_ret["anomaly"])

ax.set_xlim([0, 100])

(0.0, 100.0)

# Check that relevant periods of financial stress have been correctly classified

pd_bbva_ret["Date"] = pd.to_datetime(pd_bbva_ret["Date"]).dt.date

# Define event dates

event_dates = [

pd.to_datetime("2020-03-16").date(), # COVID lockdown Spain

pd.to_datetime("2016-06-24").date(), # Brexit referendum (first trading day)

pd.to_datetime("2016-11-09").date() # Trump election (first trading day after)

]

# Filter rows that match event dates

events_df = pd_bbva_ret[pd_bbva_ret["Date"].isin(event_dates)][["Date", "Returns", "anomaly"]]

print(events_df)

Date Returns anomaly

214 2016-06-24 -0.161792 True

312 2016-11-09 -0.057011 True

1166 2020-03-16 -0.133684 True

Example 3: Local Level Model#

import numpy as np

import matplotlib.pyplot as plt

import pandas as pd

%matplotlib inline

def simulate_local_level(T=200, sigma_v2=1.0, sigma_w2=0.05, seed=42):

rng = np.random.default_rng(seed)

y = np.zeros(T)

x = np.zeros(T)

y[0] = rng.normal(0.0, np.sqrt(sigma_w2))

x[0] = y[0] + rng.normal(0.0, np.sqrt(sigma_v2))

for t in range(1, T):

y[t] = y[t-1] + rng.normal(0.0, np.sqrt(sigma_w2))

x[t] = y[t] + rng.normal(0.0, np.sqrt(sigma_v2))

return x, y

def kf_rts_identity_cross(x, sigma_v2, sigma_w2, m0=0.0, P0=1e6):

T = len(x)

m_pred = np.zeros(T)

P_pred = np.zeros(T)

m_filt = np.zeros(T)

P_filt = np.zeros(T)

K = np.zeros(T)

innov = np.zeros(T)

S = np.zeros(T)

m_prev, P_prev = m0, P0

loglik = 0.0

for t in range(T):

# predict

m_pred[t] = m_prev

P_pred[t] = P_prev + sigma_w2

# update

innov[t] = x[t] - m_pred[t]

S[t] = P_pred[t] + sigma_v2

K[t] = P_pred[t] / S[t]

m_filt[t] = m_pred[t] + K[t] * innov[t]

P_filt[t] = (1 - K[t]) * P_pred[t]

# log-likelihood

loglik += -0.5 * (np.log(2*np.pi*S[t]) + innov[t]**2 / S[t])

m_prev, P_prev = m_filt[t], P_filt[t]

# RTS smoother

m_smooth = np.zeros(T)

P_smooth = np.zeros(T)

J = np.zeros(T-1)

m_smooth[-1] = m_filt[-1]

P_smooth[-1] = P_filt[-1]

for t in range(T-2, -1, -1):

J[t] = P_filt[t] / P_pred[t+1]

m_smooth[t] = m_filt[t] + J[t] * (m_smooth[t+1] - m_pred[t+1])

P_smooth[t] = P_filt[t] + J[t]**2 * (P_smooth[t+1] - P_pred[t+1])

# lag-one smoothed covariance via identity: P_{t-1,t|T} = J_{t-1} P_{t|T}

P_cross = np.zeros(T-1)

for t in range(1, T):

P_cross[t-1] = J[t-1] * P_smooth[t]

return {

"m_pred": m_pred, "P_pred": P_pred,

"m_filt": m_filt, "P_filt": P_filt,

"m_smooth": m_smooth, "P_smooth": P_smooth,

"innov": innov, "S": S, "K": K, "J": J,

"P_cross": P_cross, "loglik": loglik

}

def em_local_level(x, sigma_v2_init=2.0, sigma_w2_init=0.2, m0=0.0, P0=1e6, max_iter=500, tol=1e-8):

sigma_v2, sigma_w2 = float(sigma_v2_init), float(sigma_w2_init)

ll_hist = []

for it in range(max_iter):

out = kf_rts_identity_cross(x, sigma_v2, sigma_w2, m0, P0)

mu, P, Pc = out["m_smooth"], out["P_smooth"], out["P_cross"]

ll_hist.append(out["loglik"])

# E-step expectations

E1 = (x - mu)**2 + P

diff_mu = mu[1:] - mu[:-1]

E2 = diff_mu**2 + P[1:] + P[:-1] - 2.0 * Pc

# M-step (MLE scaling)

sigma_v2_new = max(np.mean(E1), 1e-12)

sigma_w2_new = max(np.mean(E2), 1e-12)

# convergence

rel = max(abs(sigma_v2_new - sigma_v2) / (sigma_v2 + 1e-12),

abs(sigma_w2_new - sigma_w2) / (sigma_w2 + 1e-12))

sigma_v2, sigma_w2 = sigma_v2_new, sigma_w2_new

if rel < tol:

ll_hist.append(kf_rts_identity_cross(x, sigma_v2, sigma_w2, m0, P0)["loglik"])

break

return {"sigma_v2": sigma_v2, "sigma_w2": sigma_w2, "ll_history": np.array(ll_hist)}

# --- Configuration ---

T = 200

sigma_v2_true = 1.0

sigma_w2_true = 0.05

seed = 42

# EM seeds

sigma_v2_init = 2.0

sigma_w2_init = 0.2

# --- Simulate ---

x, y = simulate_local_level(T, sigma_v2_true, sigma_w2_true, seed)

# --- Run EM ---

em = em_local_level(x, sigma_v2_init=sigma_v2_init, sigma_w2_init=sigma_w2_init, max_iter=1000, tol=1e-5)

sigma_v2_hat, sigma_w2_hat = em["sigma_v2"], em["sigma_w2"]

ll = em["ll_history"]

# --- Smooth with estimated params ---

out = kf_rts_identity_cross(x, sigma_v2_hat, sigma_w2_hat)

# --- Compare parameters ---

df = pd.DataFrame({

"Parameter": [r"$\sigma_v^2$", r"$\sigma_w^2$"],

"True": [sigma_v2_true, sigma_w2_true],

"EM estimate": [sigma_v2_hat, sigma_w2_hat],

})

df

| Parameter | True | EM estimate | |

|---|---|---|---|

| 0 | $\sigma_v^2$ | 1.00 | 0.871882 |

| 1 | $\sigma_w^2$ | 0.05 | 0.054226 |

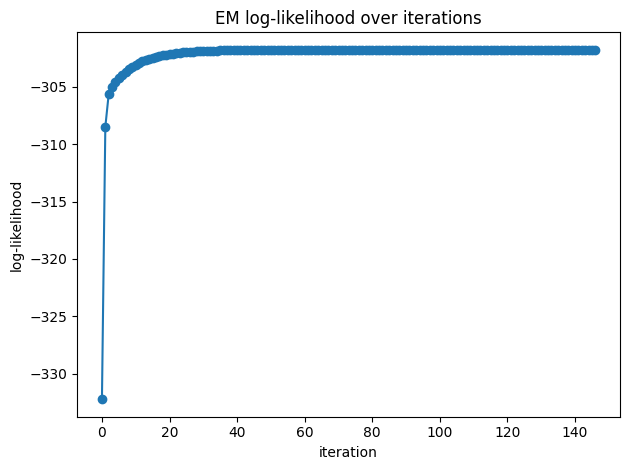

# Log-likelihood (should be non-decreasing up to numerical noise)

plt.figure()

plt.plot(ll, marker="o")

plt.title("EM log-likelihood over iterations")

plt.xlabel("iteration"); plt.ylabel("log-likelihood")

plt.tight_layout()

plt.show()

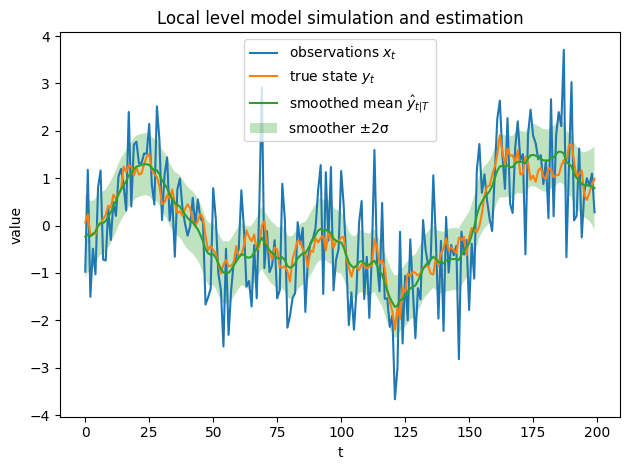

# Data and smoothed state with ±1σ band

t = np.arange(len(x))

m = out["m_smooth"]

std = np.sqrt(out["P_smooth"])

plt.figure()

plt.plot(x, label="observations $x_t$")

plt.plot(y, label="true state $y_t$")

plt.plot(m, label="smoothed mean $\hat{y}_{t|T}$")

plt.fill_between(t, m - 2*std, m + 2*std, alpha=0.3, facecolor="tab:green",

edgecolor="none", zorder=0,label="smoother ±2σ")

plt.legend()

plt.title("Local level model simulation and estimation")

plt.xlabel("t"); plt.ylabel("value")

plt.tight_layout()

plt.show()

<>:17: SyntaxWarning: invalid escape sequence '\h'

<>:17: SyntaxWarning: invalid escape sequence '\h'

/var/folders/d5/k0x6wwx97k7_73_1cz5q38t40000gn/T/ipykernel_39762/1804985963.py:17: SyntaxWarning: invalid escape sequence '\h'

plt.plot(m, label="smoothed mean $\hat{y}_{t|T}$")