Modelling RfQs in Dealer to Client Markets#

Generative models for the request for quote activity#

Simulation of RfQs arrival and client attrition#

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from scipy.stats import poisson, norm

from collections import deque

def run_simulation(N_clients=50,

T=200,

reservation_price_mean=100,

reservation_price_std_pct=0.1,

lambda_mean=1,

lambda_std=0.05,

prior_mean=60,

prior_std=10,

res_price_noise_std_pct=0.2,

hit_rate_target=0.4,

window_size=10,

attrition_threshold=0.1):

"""

Simulate RFQ interactions with Bayesian quantile pricing and client attrition.

Clients stop trading if their moving-average hit rate over `window_size` days falls below `attrition_threshold`.

Returns:

rfq_df: DataFrame of RfQ events

active_history: list of active client counts per day

activity_matrix: binary DataFrame of daily activity (clients x days)

"""

np.random.seed(42)

# Generate distribution of reservation prices for the segment of clients

reservation_prices = np.random.normal(reservation_price_mean,

reservation_price_mean * reservation_price_std_pct,

N_clients)

# Reservation prices are noisy given potential changing market conditions

res_price_noise_std = res_price_noise_std_pct * reservation_price_mean

res_price_noise_var = res_price_noise_std**2

# Generate distribution of RfQ intensities for the segment of clients

lambdas = np.abs(np.random.normal(lambda_mean, lambda_std, N_clients))

clients_posterior = {i: {'mean': prior_mean, 'var': prior_std**2,

'n': 0, 'sum_obs': 0.0}

for i in range(N_clients)}

z = norm.ppf(1 - hit_rate_target)

active = np.ones(N_clients, dtype=bool)

# Track per-client active status at end of each day

active_flags = np.zeros((T, N_clients), dtype=bool)

daily_history = [deque(maxlen=window_size) for _ in range(N_clients)]

active_history = []

records = []

Y = np.zeros((T, N_clients), dtype=int)

for t in range(T):

daily_hits = np.zeros(N_clients, dtype=int)

daily_reqs = np.zeros(N_clients, dtype=int)

for i in range(N_clients):

if not active[i]: continue

n_rfq = poisson.rvs(lambdas[i])

if n_rfq > 0: Y[t,i] = 1

for _ in range(n_rfq):

post = clients_posterior[i]

price = max(0.0, post['mean'] + np.sqrt(post['var'] + res_price_noise_var) * z)

r = norm.rvs(reservation_prices[i], res_price_noise_std)

# Trading happens when price offered is lower than the reservation price

hit = price <= r

daily_reqs[i] += 1; daily_hits[i] += int(hit)

# The dealer updates the estimation of the reservation price of the client

post['n'] += 1; post['sum_obs'] += r

post_var = 1/(1/prior_std**2 + post['n']/res_price_noise_var)

post['var'] = post_var

post['mean'] = post_var*(prior_mean/prior_std**2 + post['sum_obs']/res_price_noise_var)

records.append({'time': t, 'client_id': i, 'price': price, 'hit': hit})

for i in range(N_clients):

if not active[i] or daily_reqs[i]==0: continue

rate = daily_hits[i]/daily_reqs[i]

daily_history[i].append(rate)

# A client stops sending RfQs to the dealer if the hit & miss is too low

if len(daily_history[i])==window_size and np.mean(daily_history[i])<attrition_threshold:

active[i] = False

active_history.append(active.sum())

active_flags[t, :] = active.copy()

rfq_df = pd.DataFrame(records)

activity = pd.DataFrame(Y, columns=[f'client_{i}' for i in range(N_clients)])

active_df = pd.DataFrame(active_flags, columns=[f'client_{i}' for i in range(N_clients)])

return rfq_df, active_history, activity, active_df

from scipy.special import betaln

from scipy.optimize import minimize

# ----------------------

# Segment-level Model

# ----------------------

def estimate_segment_params(activity_matrix):

def log_marginal_likelihood(D, alpha, beta, gamma, delta):

n, x = len(D), D.sum()

last = np.where(D==1)[0]

r = n - (last[-1]+1) if last.size>0 else n

logA = (betaln(alpha+x, beta+n-x)-betaln(alpha,beta)

+betaln(gamma, delta+n)-betaln(gamma,delta))

logB = [(betaln(alpha+x, beta+n-x-i)-betaln(alpha,beta)

+betaln(gamma+1, delta+n-i)-betaln(gamma,delta))

for i in range(1, r+1)]

mags = [logA] + logB; m_max = max(mags)

return m_max + np.log(sum(np.exp(m - m_max) for m in mags))

def neg_ll(params):

alpha, beta, gamma, delta = np.exp(params)

return -sum(log_marginal_likelihood(activity_matrix.iloc[:end, j].values,

alpha, beta, gamma, delta)

for j in range(activity_matrix.shape[1])

for end in [activity_matrix.iloc[:,:].values.shape[0]])

res = minimize(neg_ll, np.log([1,1,1,1]), method='L-BFGS-B', bounds=[(-5,5)]*4)

return np.exp(res.x)

def attrition_probability(D, alpha, beta, gamma, delta):

n, x = len(D), D.sum()

last = np.where(D==1)[0]

r = n - (last[-1]+1) if last.size>0 else n

logA = (betaln(alpha+x, beta+n-x)-betaln(alpha,beta)

+betaln(gamma, delta+n)-betaln(gamma,delta))

logB = [(betaln(alpha+x, beta+n-x-i)-betaln(alpha,beta)

+betaln(gamma+1, delta+n-i)-betaln(gamma,delta))

for i in range(1, r+1)]

mags = [logA] + logB; m_max = max(mags)

logL = m_max + np.log(sum(np.exp(m - m_max) for m in mags))

P_active = np.exp(logA - logL)

return 1 - P_active

from sklearn.metrics import (

confusion_matrix, accuracy_score,

precision_score, recall_score,

roc_curve, auc

)

# ----------------------

# Workflow: Simulate, Train, Test

# ----------------------

T_train, T_test = 100, 100

T_tot = T_train + T_test

N_clients = 50

rfq_all, active_all, Y_all, active_df = run_simulation(N_clients = N_clients, T=T_train+T_test)

Y_train = Y_all.iloc[:T_train].reset_index(drop=True)

Y_test = Y_all.iloc[T_train:].reset_index(drop=True)

rfq_test = rfq_all[rfq_all['time']>=T_train].copy()

rfq_test['time'] -= T_train

active_test = active_all[T_train:]

alpha, beta, gamma, delta = estimate_segment_params(Y_train)

print(f"Params: α={alpha:.2f}, β={beta:.2f}, γ={gamma:.2f}, δ={delta:.2f}")

# ----------------------

# Risk Scoring

# ----------------------

risk_records = []

for j in range(Y_test.shape[1]):

hist = []

for t in range(T_test):

hist.append(Y_test.iloc[t, j])

D = np.array(hist, dtype=int)

p_inact = attrition_probability(D, alpha, beta, gamma, delta)

risk_records.append({

'time': t,

'client_id': j,

'p_inactive': p_inact,

'alert': p_inact > 0.5 # thresholded prediction

})

risk_df = pd.DataFrame(risk_records)

# Label inactivity

risk_df['inactive'] = risk_df.apply(

lambda r: not active_df.loc[r['time'] + T_train, f'client_{r["client_id"]}'],

axis=1

)

# ----------------------

# Evaluation Metrics

# ----------------------

# Ground truth and predictions

y_true = risk_df['inactive']

y_pred = risk_df['alert'] # at 0.5 threshold

y_scores = risk_df['p_inactive'] # raw probabilities

# Confusion matrix

tn, fp, fn, tp = confusion_matrix(y_true, y_pred).ravel()

print("Confusion Matrix:")

print(f" TN={tn}, FP={fp}, FN={fn}, TP={tp}")

# Accuracy, Precision, Recall at 0.5

accuracy = accuracy_score(y_true, y_pred)

precision = precision_score(y_true, y_pred)

recall = recall_score(y_true, y_pred)

print(f"Accuracy : {accuracy:.4f}")

print(f"Precision: {precision:.4f}")

print(f"Recall : {recall:.4f}")

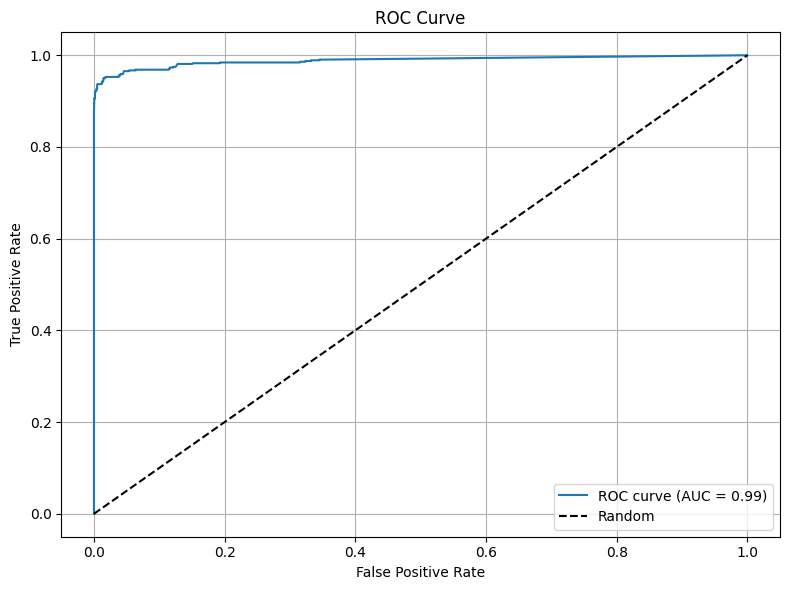

# ROC curve & AUC

fpr, tpr, thresholds = roc_curve(y_true, y_scores)

roc_auc = auc(fpr, tpr)

print(f"AUC : {roc_auc:.4f}")

# Plot ROC

plt.figure(figsize=(8, 6))

plt.plot(fpr, tpr, label=f'ROC curve (AUC = {roc_auc:.2f})')

plt.plot([0, 1], [0, 1], 'k--', label='Random')

plt.xlabel('False Positive Rate')

plt.ylabel('True Positive Rate')

plt.title('ROC Curve')

plt.legend(loc='lower right')

plt.grid(True)

plt.tight_layout()

plt.show()

Params: α=148.41, β=85.31, γ=0.08, δ=148.41

Confusion Matrix:

TN=4365, FP=0, FN=76, TP=559

Accuracy : 0.9848

Precision: 1.0000

Recall : 0.8803

AUC : 0.9884

# ----------------------

# Plots: Hit Rate & Attrition Over Full Simulation

# ----------------------

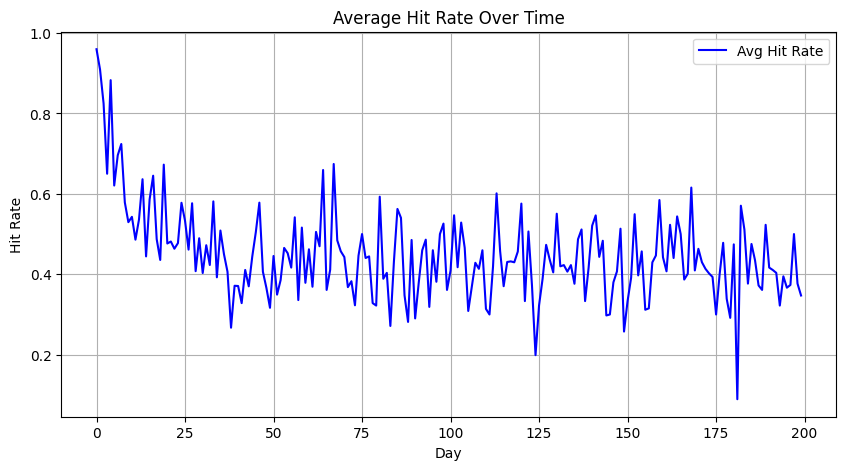

# Active-client hit rate over time

hit_rate_active = []

days = np.arange(T_tot)

for t in days:

act_clients = active_df.iloc[t]

active_ids = [int(col.split('_')[1]) for col, flag in act_clients.items() if flag]

daily = rfq_all[rfq_all['time'] == t]

rates = []

for cid in active_ids:

cr = daily[daily['client_id'] == cid]

if not cr.empty:

rates.append(cr['hit'].mean())

hit_rate_active.append(np.mean(rates) if rates else np.nan)

plt.figure(figsize=(10,5))

plt.plot(days, hit_rate_active, label='Avg Hit Rate', color='blue')

plt.title('Average Hit Rate Over Time')

plt.xlabel('Day'); plt.ylabel('Hit Rate'); plt.grid(True); plt.legend()

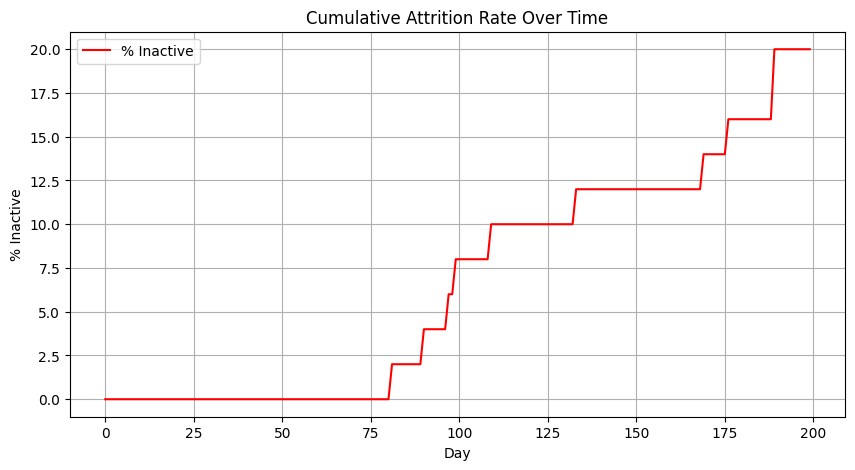

# Attrition rate over time

attr_rate = [100 * (Y_all.shape[1] - x) / Y_all.shape[1] for x in active_all]

plt.figure(figsize=(10,5))

plt.plot(days, attr_rate, label='% Inactive', color='red')

plt.title('Cumulative Attrition Rate Over Time')

plt.xlabel('Day'); plt.ylabel('% Inactive'); plt.grid(True); plt.legend()

<matplotlib.legend.Legend at 0x31037edf0>

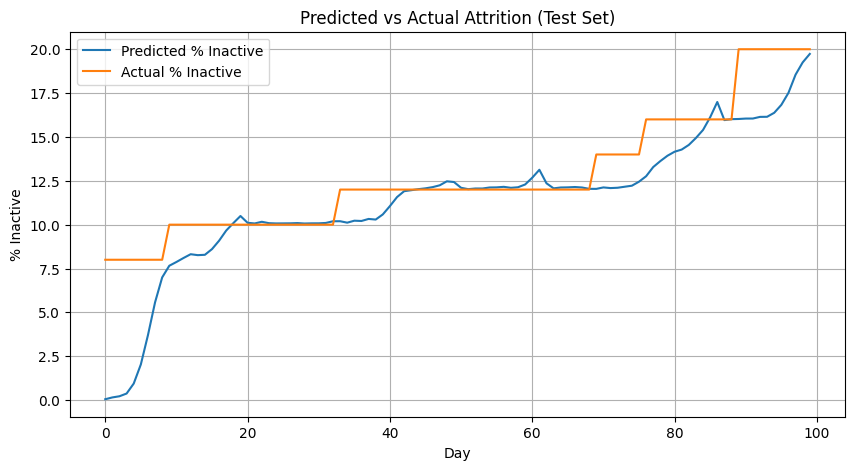

# ----------------------

# Model Fit Visualization

# ----------------------

# Compare predicted attrition vs actual on test

pred_rate = risk_df.groupby('time')['p_inactive'].mean()

actual_rate = [100*(N_clients-x)/N_clients for x in active_test]

plt.figure(figsize=(10,5))

plt.plot(pred_rate.index, 100*pred_rate.values, label='Predicted % Inactive')

plt.plot(actual_rate, label='Actual % Inactive')

plt.title('Predicted vs Actual Attrition (Test Set)')

plt.xlabel('Day'); plt.ylabel('% Inactive'); plt.legend(); plt.grid(True)

import numpy as np

import matplotlib.pyplot as plt

# ----------------------

# Function: Plot Clients by ID (single figure with subplots)

# ----------------------

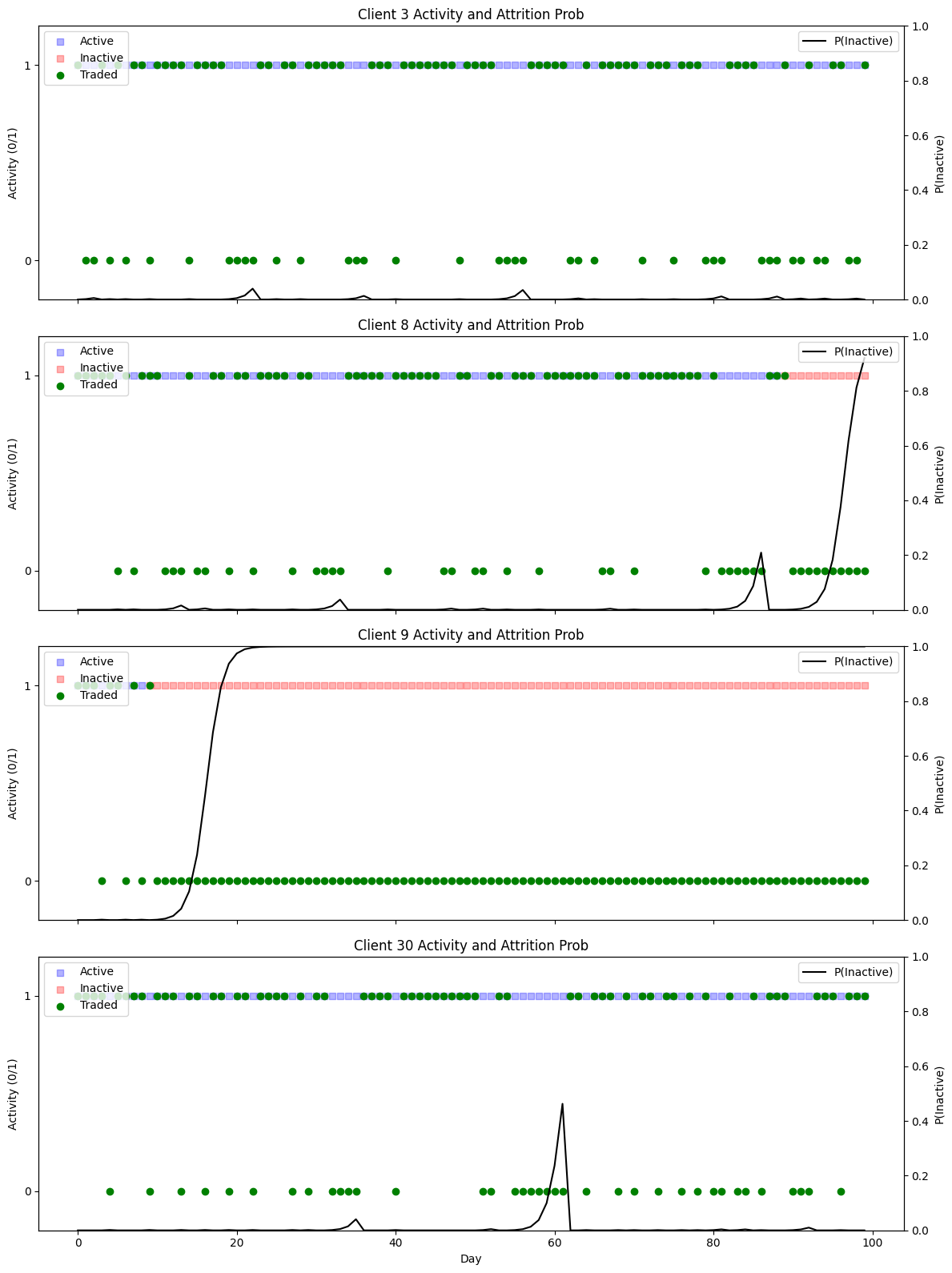

def plot_clients_subplots(client_ids):

"""

For each client in client_ids, create a subplot in one figure:

- Left y-axis: active (blue=active, red=inactive) and trading days (green), with numeric ticks (0/1)

- Right y-axis: attrition probability over time

- Separate legends: left for 'Active', 'Inactive', 'Traded'; right for 'P(Inactive)'

- Title of each subplot shows the client ID

"""

n = len(client_ids)

fig, axes = plt.subplots(nrows=n, ncols=1, figsize=(12, 4*n), sharex=True)

if n == 1:

axes = [axes]

days = np.arange(T_test)

for ax1, cid in zip(axes, client_ids):

# gather P(inactive) values

p_vals = [

risk_df.loc[

(risk_df['client_id'] == cid) & (risk_df['time'] == t),

'p_inactive'

].item()

for t in days

]

# latent active flags and trading days

active_flag = active_df[T_train:][f'client_{cid}'].values

trade_days = Y_test.iloc[:, cid]

# Left axis: Active vs Inactive

idx_active = days[active_flag]

idx_inactive = days[~active_flag]

h_active = ax1.scatter(idx_active, [1]*len(idx_active), c='blue', marker='s', alpha=0.3, label='Active')

h_inactive = ax1.scatter(idx_inactive, [1]*len(idx_inactive), c='red', marker='s', alpha=0.3, label='Inactive')

# Left axis: actual trades (0 or 1)

h_trade = ax1.scatter(trade_days.index, trade_days.values,

c='green', marker='o', label='Traded')

# Set numeric ticks on left y-axis

ax1.set_ylim(-0.2, 1.2)

ax1.set_yticks([0, 1])

ax1.set_ylabel('Activity (0/1)')

ax1.set_title(f'Client {cid} Activity and Attrition Prob')

# Left-axis legend

ax1.legend(handles=[h_active, h_inactive, h_trade],

labels=['Active', 'Inactive', 'Traded'],

loc='upper left')

# Right axis: P(Inactive)

ax2 = ax1.twinx()

h_prob, = ax2.plot(days, p_vals, c='black', label='P(Inactive)')

ax2.set_ylim(0, 1)

ax2.set_ylabel('P(Inactive)')

# Right-axis legend

ax2.legend(handles=[h_prob], loc='upper right')

axes[-1].set_xlabel('Day')

plt.tight_layout()

plt.show()

# Example: plot select clients in one figure

#plot_clients_subplots([3, 8, 9, 18])

plot_clients_subplots([3, 8, 9, 30])

Simulation of client abnormal behavior#

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from scipy.stats import poisson, norm

from collections import deque

def run_simulation(N_clients=50,

T=200,

reservation_price_mean=100,

reservation_price_std_pct=0.1,

lambda_mean=1,

lambda_std=0.05,

prior_mean=60,

prior_std=10,

reservation_price_noise_std=None,

discount_trigger_pct=0.35, # trigger threshold: 0.5 means 50% lower

boosted_rate_factor = 10,

hit_rate_target=0.4,

window_size=10,

attrition_threshold=0.1,

random_seed=42):

"""

Simulate RFQ interactions with Bayesian quantile pricing and client attrition.

Adds a mechanism: if a client gets a quote at least `discount_trigger_pct` below their reservation price,

they double their RFQ rate until the dealer quotes above their reservation price.

"""

np.random.seed(random_seed)

# Generate distribution of reservation prices

reservation_prices = np.random.normal(reservation_price_mean,

reservation_price_mean * reservation_price_std_pct,

N_clients)

# Noise in reservation prices

fair_price = reservation_price_mean

res_price_noise_std = reservation_price_noise_std or (fair_price * reservation_price_std_pct * 2)

res_price_noise_var = res_price_noise_std ** 2

# Base RfQ intensities

lambdas = np.abs(np.random.normal(lambda_mean, lambda_std, N_clients))

base_lambdas = lambdas.copy() # store for reset later

# Posterior beliefs

clients_posterior = {i: {'mean': prior_mean, 'var': prior_std ** 2,

'n': 0, 'sum_obs': 0.0}

for i in range(N_clients)}

z = norm.ppf(1 - hit_rate_target)

active = np.ones(N_clients, dtype=bool)

# Flags for tracking "boosted" mode

boosted = np.zeros(N_clients, dtype=bool)

# Track daily active/boosted status

active_flags = np.zeros((T, N_clients), dtype=bool)

boosted_flags = np.zeros((T, N_clients), dtype=bool)

daily_history = [deque(maxlen=window_size) for _ in range(N_clients)]

active_history = []

records = []

Y = np.zeros((T, N_clients), dtype=int) # binary: whether client sent at least one RFQ that day

for t in range(T):

daily_hits = np.zeros(N_clients, dtype=int)

daily_reqs = np.zeros(N_clients, dtype=int)

for i in range(N_clients):

if not active[i]:

continue

n_rfq = poisson.rvs(lambdas[i])

if n_rfq > 0:

Y[t, i] = 1

for _ in range(n_rfq):

post = clients_posterior[i]

price = max(0.0, post['mean'] + np.sqrt(post['var'] + res_price_noise_var) * z)

r = norm.rvs(reservation_prices[i], res_price_noise_std)

# Trading happens when price <= reservation price

hit = price <= r

daily_reqs[i] += 1

daily_hits[i] += int(hit)

# Check discount trigger

if price <= (1 - discount_trigger_pct) * r:

boosted[i] = True

lambdas[i] = base_lambdas[i] * boosted_rate_factor

elif boosted[i] and price > r / (1-discount_trigger_pct):

boosted[i] = False

lambdas[i] = base_lambdas[i]

# Update posterior belief

post['n'] += 1

post['sum_obs'] += r

post_var = 1 / (1 / (prior_std ** 2) + post['n'] / res_price_noise_var)

post['var'] = post_var

post['mean'] = post_var * (prior_mean / (prior_std ** 2) +

post['sum_obs'] / res_price_noise_var)

records.append({'time': t,

'client_id': i,

'price': price,

'reservation': r,

'hit': hit,

'boosted': boosted[i]})

# Update attrition status

for i in range(N_clients):

if not active[i] or daily_reqs[i] == 0:

continue

rate = daily_hits[i] / daily_reqs[i]

daily_history[i].append(rate)

if len(daily_history[i]) == window_size and np.mean(daily_history[i]) < attrition_threshold:

active[i] = False

active_history.append(int(active.sum()))

active_flags[t, :] = active.copy()

boosted_flags[t, :] = boosted.copy()

rfq_df = pd.DataFrame(records)

activity_df = pd.DataFrame(Y, columns=[f'client_{i}' for i in range(N_clients)])

active_df = pd.DataFrame(active_flags, columns=[f'client_{i}' for i in range(N_clients)])

boosted_df = pd.DataFrame(boosted_flags, columns=[f'client_{i}' for i in range(N_clients)])

return rfq_df, active_history, activity_df, active_df, boosted_df

# Run simulation

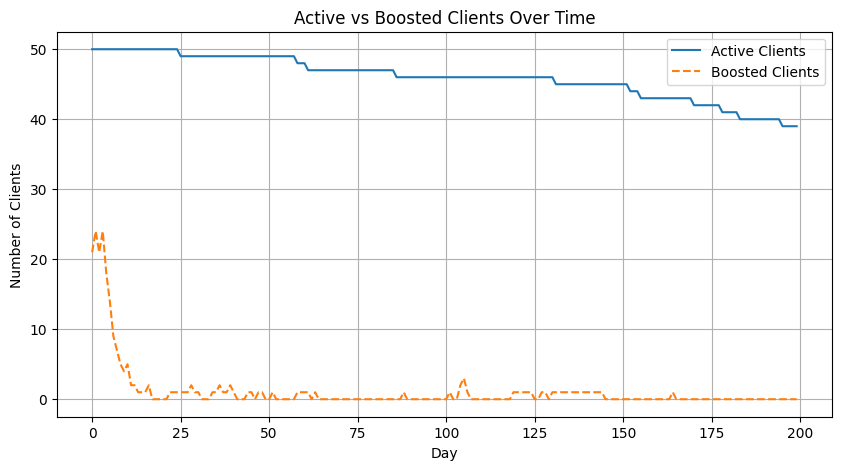

rfq_df, active_history, activity_df, active_df, boosted_df = run_simulation()

# Plot active and boosted clients over time

plt.figure(figsize=(10,5))

plt.plot(active_df.sum(axis=1), label='Active Clients')

plt.plot(boosted_df.sum(axis=1), label='Boosted Clients', linestyle='--')

plt.xlabel('Day')

plt.ylabel('Number of Clients')

plt.title('Active vs Boosted Clients Over Time')

plt.legend()

plt.grid(True)

plt.show()

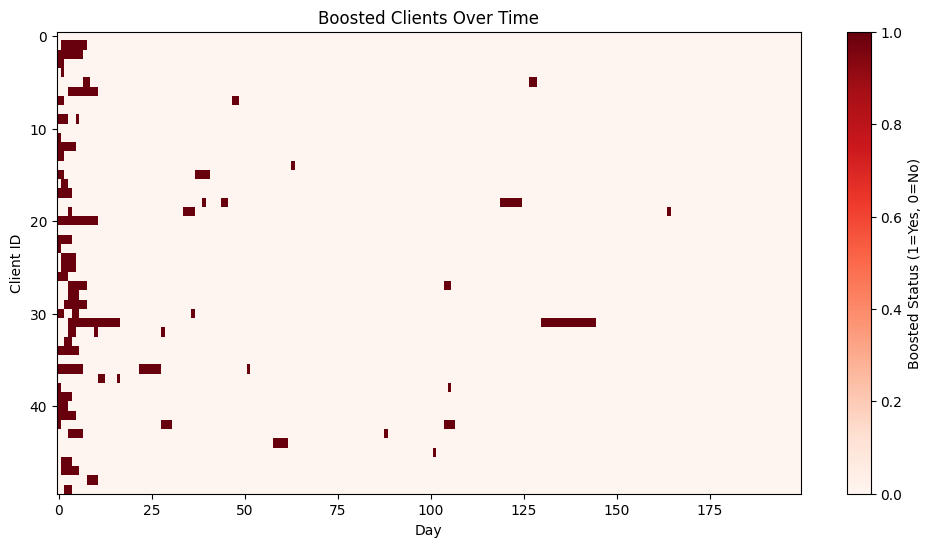

# Heatmap of boosted status

plt.figure(figsize=(12,6))

plt.imshow(boosted_df.T, aspect='auto', cmap='Reds')

plt.colorbar(label='Boosted Status (1=Yes, 0=No)')

plt.xlabel('Day')

plt.ylabel('Client ID')

plt.title('Boosted Clients Over Time')

plt.show()

from scipy.special import betaln, gammaln

from scipy.optimize import minimize

# -----------------------------

# Beta-Binomial mixture MLE with shared mean

# -----------------------------

def log_beta_binom_pmf(x, n, alpha, beta):

# log [ C(n,x) * B(alpha+x, beta+n-x) / B(alpha,beta) ]

return (

gammaln(n + 1) - gammaln(x + 1) - gammaln(n - x + 1)

+ betaln(alpha + x, beta + n - x)

- betaln(alpha, beta)

)

def neg_log_likelihood(params, xs, ns):

# params = [logit_mu, log_k_g, log_k_b, logit_qg]

logit_mu, log_k_g, log_k_b, logit_qg = params

mu = 1 / (1 + np.exp(-logit_mu)) # shared mean

k_g = np.exp(log_k_g) + 1e-8

k_b = np.exp(log_k_b) + 1e-8

qg = 1 / (1 + np.exp(-logit_qg))

# convert to alpha, beta

alpha_g, beta_g = mu * k_g, (1 - mu) * k_g

alpha_b, beta_b = mu * k_b, (1 - mu) * k_b

# mixture likelihood per client

ll = []

for x, n in zip(xs, ns):

log_p_g = log_beta_binom_pmf(x, n, alpha_g, beta_g)

log_p_b = log_beta_binom_pmf(x, n, alpha_b, beta_b)

# log-sum-exp for mixture

a = np.log(qg) + log_p_g

b = np.log(1 - qg) + log_p_b

m = max(a, b)

ll_i = m + np.log(np.exp(a - m) + np.exp(b - m))

ll.append(ll_i)

return -np.sum(ll)

def fit_beta_mixture_mle(activity_df, train_days):

"""

activity_df: (T x N) binary DataFrame

train_days: number of days used for training (first half)

Returns dict with fitted parameters.

"""

T, N = activity_df.shape

A = activity_df.iloc[:train_days].values # (train_days x N)

xs = A.sum(axis=0) # successes per client in training

ns = np.full_like(xs, fill_value=train_days)

# rough start for mean

p_hat = xs.mean() / train_days

logit_mu0 = np.log(p_hat / (1 - p_hat + 1e-8))

start = np.array([

logit_mu0,

np.log(10.0), # k_g initial concentration

np.log(2.0), # k_b initial concentration

0.0 # logit(0.5)

], dtype=float)

res = minimize(neg_log_likelihood, start, args=(xs, ns), method='L-BFGS-B')

logit_mu, log_k_g, log_k_b, logit_qg = res.x

mu = 1 / (1 + np.exp(-logit_mu))

k_g = np.exp(log_k_g) + 1e-8

k_b = np.exp(log_k_b) + 1e-8

params = {

'mu': float(mu),

'alpha_g': float(mu * k_g), 'beta_g': float((1 - mu) * k_g),

'alpha_b': float(mu * k_b), 'beta_b': float((1 - mu) * k_b),

'q_g': float(1 / (1 + np.exp(-logit_qg))),

'success': bool(res.success),

'message': res.message

}

return params

def posterior_good(x, n, params):

a_g = params['alpha_g']; b_g = params['beta_g']

a_b = params['alpha_b']; b_b = params['beta_b']

q_g = params['q_g']

log_p_g = log_beta_binom_pmf(x, n, a_g, b_g)

log_p_b = log_beta_binom_pmf(x, n, a_b, b_b)

a = np.log(q_g) + log_p_g

b = np.log(1 - q_g) + log_p_b

m = max(a, b)

num = np.exp(a - m)

den = num + np.exp(b - m)

return float(num / den)

# Fit on first half, removing first 25 days until it settles

T = activity_df.shape[0]

mid = T // 2

params = fit_beta_mixture_mle(activity_df[25:], train_days=mid)

# Detect abnormalities on second half using a sliding window

n_window = 10 # window size for detection, can be adjusted

threshold = 0.5 # classify as abnormal if p(good|D) < threshold

N = activity_df.shape[1]

abnormal_flags = np.zeros_like(activity_df.values, dtype=bool)

# For each day t in the second half, use the last n_window days (bounded within the second half)

for t in range(mid, T):

start = max(mid, t - n_window + 1)

end = t + 1

window = activity_df.iloc[start:end].values # (w x N)

n = window.shape[0]

x = window.sum(axis=0)

# Posterior for each client

p_good = np.array([posterior_good(int(xi), int(n), params) for xi in x])

abnormal_flags[t, :] = p_good < threshold

abnormal_df = pd.DataFrame(abnormal_flags, columns=activity_df.columns, index=activity_df.index)

params

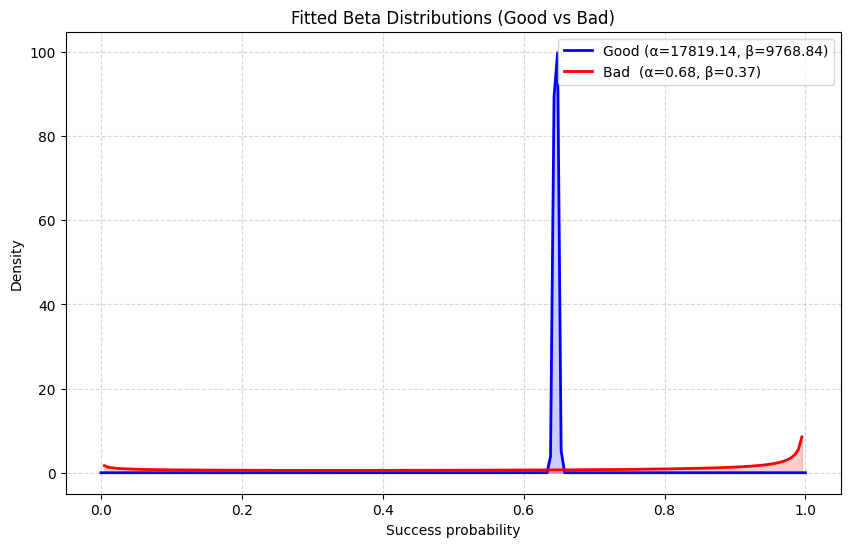

{'mu': 0.6459024041525655,

'alpha_g': 17819.14219878137,

'beta_g': 9768.837168102045,

'alpha_b': 0.6772910514791353,

'beta_b': 0.3713055277018204,

'q_g': 0.892871535754001,

'success': True,

'message': 'CONVERGENCE: REL_REDUCTION_OF_F_<=_FACTR*EPSMCH'}

import numpy as np

import matplotlib.pyplot as plt

from scipy.stats import beta

def plot_fitted_betas(params, bins=200):

"""

Plot fitted good vs bad Beta distributions.

params: dict returned by fit_beta_mixture_mle

"""

a_g, b_g = params['alpha_g'], params['beta_g']

a_b, b_b = params['alpha_b'], params['beta_b']

q_g = params['q_g']

# Grid

x = np.linspace(0, 1, bins)

# Densities

pdf_g = beta.pdf(x, a_g, b_g)

pdf_b = beta.pdf(x, a_b, b_b)

plt.figure(figsize=(10, 6))

plt.plot(x, pdf_g, label=f"Good (α={a_g:.2f}, β={b_g:.2f})", lw=2, color="blue")

plt.plot(x, pdf_b, label=f"Bad (α={a_b:.2f}, β={b_b:.2f})", lw=2, color="red")

plt.fill_between(x, pdf_g, alpha=0.2, color="blue")

plt.fill_between(x, pdf_b, alpha=0.2, color="red")

plt.title("Fitted Beta Distributions (Good vs Bad)")

plt.xlabel("Success probability")

plt.ylabel("Density")

plt.legend()

plt.grid(True, ls="--", alpha=0.5)

plt.show()

plot_fitted_betas(params)

# Use a previous window (exclude day t) when computing P(good|D)

n_window = 10

threshold = 0.5

def build_pgood_panel(activity_df, boosted_df, active_df, params, mid, n_window, threshold):

T, N = activity_df.shape

rows = []

# Start at mid + n_window to ensure a full *previous* window exists

for t in range(mid + n_window, T):

start = t - n_window

end = t # exclude day t

window = activity_df.iloc[start:end] # (n_window x N)

x = window.sum(axis=0).values.astype(int) # successes per client in previous window

n = n_window

# compute p_good for each client

p_goods = []

for j in range(N):

p = posterior_good(int(x[j]), int(n), params)

p_goods.append(p)

p_goods = np.array(p_goods)

# flags at time t

boosted_t = boosted_df.iloc[t].values.astype(bool)

active_t = active_df.iloc[t].values.astype(bool)

inactive_t = ~active_t

traded_today = activity_df.iloc[t].values.astype(int)

for j in range(N):

rows.append({

'day': t,

'client_id': j,

'x': int(x[j]),

'n': int(n),

'p_good': float(p_goods[j]),

'abnormal': bool(p_goods[j] < threshold),

'boosted': bool(boosted_t[j]),

'inactive': bool(inactive_t[j]),

'traded_today': int(traded_today[j])

})

panel = pd.DataFrame(rows)

return panel

panel_df = build_pgood_panel(activity_df, boosted_df, active_df, params, mid, n_window, threshold)

# Correctly aligned daily summary for second half *with windowing*

days = sorted(panel_df['day'].unique())

daily_summary = panel_df.groupby('day').agg(

abnormal_count=('abnormal', 'sum'),

boosted_count=('boosted', 'sum'),

inactive_count=('inactive', 'sum')

).reset_index()

# Overlap summary on client-day panel

overlap_summary = {

'days_evaluated': int(len(days)),

'clients': int(N),

'total_client_days': int(panel_df.shape[0]),

'abnormal_client_days': int(panel_df['abnormal'].sum()),

'boosted_client_days': int(panel_df['boosted'].sum()),

'inactive_client_days': int(panel_df['inactive'].sum()),

'abnormal_and_boosted': int((panel_df['abnormal'] & panel_df['boosted']).sum()),

'abnormal_and_inactive': int((panel_df['abnormal'] & panel_df['inactive']).sum()),

'abnormal_not_boosted_or_inactive': int((panel_df['abnormal'] & ~panel_df['boosted'] & ~panel_df['inactive']).sum())

}

overlap_df2 = pd.DataFrame([overlap_summary])

# Heatmap of p_good by client (days x clients) for visual inspection

# Build a matrix with rows=days, cols=clients

days_idx = daily_summary['day'].values

pgood_mat = np.full((len(days_idx), N), np.nan)

for i, t in enumerate(days_idx):

slice_t = panel_df[panel_df['day'] == t].sort_values('client_id')

pgood_mat[i, :] = slice_t['p_good'].values

plt.figure(figsize=(12,6))

plt.imshow(pgood_mat.T, aspect='auto')

plt.colorbar(label='P(good | previous window)')

plt.xlabel('Day index in second half')

plt.ylabel('Client ID')

plt.title('Per-client P(good|D) over time (previous window)')

plt.show()

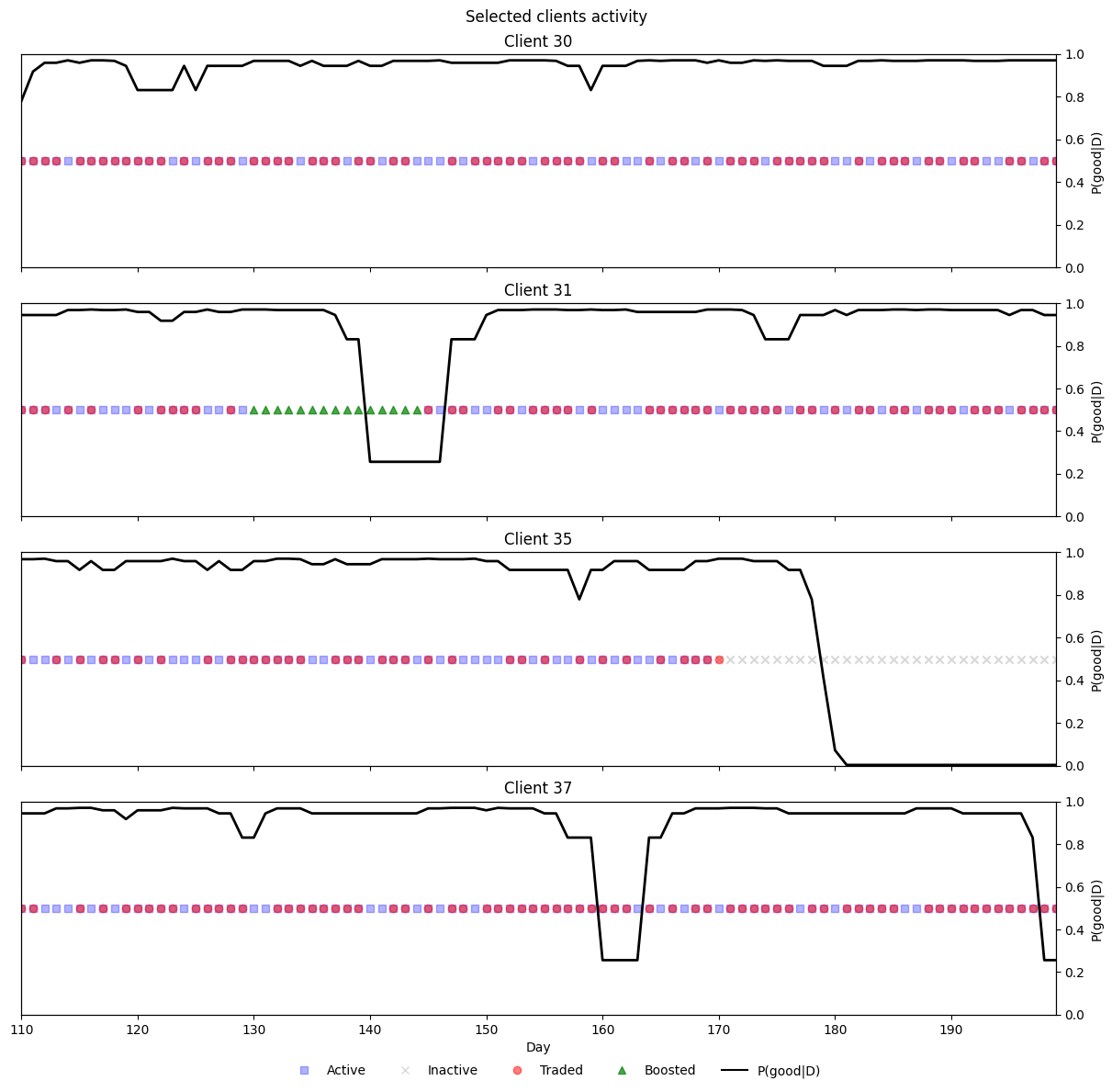

from matplotlib.lines import Line2D

def plot_clients_activity_prob(clients, df):

"""

One figure with one row per client.

On boosted days, only the 'Boosted' marker is shown (others hidden).

"""

clients = list(clients)

n = len(clients)

if n == 0:

return

fig, axes = plt.subplots(n, 1, figsize=(12, 2.8 * n), sharex=True, constrained_layout=True)

if n == 1:

axes = [axes]

# Build a single, global legend

legend_elems = [

Line2D([0],[0], marker='s', linestyle='None', color='blue', alpha=0.3, label='Active'),

Line2D([0],[0], marker='x', linestyle='None', color='gray', alpha=0.3, label='Inactive'),

Line2D([0],[0], marker='o', linestyle='None', color='red', alpha=0.5, label='Traded'),

Line2D([0],[0], marker='^', linestyle='None', color='green', alpha=0.7, label='Boosted'),

Line2D([0],[0], linestyle='-', color='black', label='P(good|D)'),

]

x_min, x_max = None, None

for ax, cid in zip(axes, clients):

df_c = df[df['client_id'] == cid].sort_values('day').copy()

if df_c.empty:

ax.set_title(f"Client {cid} (no data)")

ax.set_yticks([])

continue

# Masks

boosted_mask = df_c['boosted']

active_mask = (~df_c['inactive']) & (~boosted_mask)

inactive_mask = df_c['inactive'] & (~boosted_mask)

traded_mask = (df_c['traded_today'] == 1) & (~boosted_mask)

# Scatter statuses

ax.scatter(df_c['day'][active_mask], [1]*active_mask.sum(), c='blue', marker='s', alpha=0.3)

ax.scatter(df_c['day'][inactive_mask], [1]*inactive_mask.sum(), c='gray', marker='x', alpha=0.3)

ax.scatter(df_c['day'][traded_mask], [1]*traded_mask.sum(), c='red', marker='o', alpha=0.5)

ax.scatter(df_c['day'][boosted_mask], [1]*boosted_mask.sum(), c='green', marker='^', alpha=0.7, zorder=3)

ax.set_yticks([])

ax.set_ylim(0.5, 1.5)

# p_good

ax2 = ax.twinx()

ax2.plot(df_c['day'], df_c['p_good'], color='black', lw=2)

ax2.set_ylim(0, 1)

ax2.set_ylabel("P(good|D)")

ax.set_title(f"Client {cid}")

# Track x-lims

dmin, dmax = df_c['day'].min(), df_c['day'].max()

x_min = dmin if x_min is None else min(x_min, dmin)

x_max = dmax if x_max is None else max(x_max, dmax)

axes[-1].set_xlabel("Day")

if x_min is not None and x_max is not None:

axes[-1].set_xlim(x_min, x_max)

fig.suptitle("Selected clients activity", y=1.02)

# Move legend below figure

fig.legend(handles=legend_elems, loc='lower center', ncol=5, frameon=False, bbox_to_anchor=(0.5, -0.03))

plt.show()

plot_clients_activity_prob([30,31,35, 37], panel_df)

from sklearn.metrics import confusion_matrix

def _cm_df(cm, labels=("Pred 0", "Pred 1"), index=("True 0", "True 1")):

"""Pretty dataframe for a 2x2 confusion matrix."""

return pd.DataFrame(cm, index=index, columns=labels)

def evaluate_confusions(panel_df, normalize=False):

"""

Evaluate confusion matrices without recomputing thresholds.

Uses:

- df['abnormal'] as the model's predicted abnormal label (already thresholded).

- df['inactive'] and df['boosted'] as operational labels.

- Global abnormality = (inactive OR boosted).

Returns dict with both raw arrays and pretty DataFrames.

Set normalize=True to return per-true-class rates instead of counts.

"""

df = panel_df.copy()

# Ensure ints

y_abnormal = df["abnormal"].astype(int).values

y_inactive = df["inactive"].astype(int).values

y_boosted = df["boosted"].astype(int).values

# Global abnormality (prediction-side for the overall CM)

y_global_abn = (df["inactive"] | df["boosted"]).astype(int).values

# Normalization mode for sklearn

norm_mode = "true" if normalize else None

results = {}

# 1) Inactive (truth) vs Abnormal (model)

cm_inactive = confusion_matrix(y_inactive, y_abnormal, labels=[0,1], normalize=norm_mode)

results["inactive_vs_abnormal"] = cm_inactive

results["inactive_vs_abnormal_df"] = _cm_df(cm_inactive)

# 2) Boosted (truth) vs Abnormal (model)

cm_boosted = confusion_matrix(y_boosted, y_abnormal, labels=[0,1], normalize=norm_mode)

results["boosted_vs_abnormal"] = cm_boosted

results["boosted_vs_abnormal_df"] = _cm_df(cm_boosted)

# 3) OVERALL: Abnormal (truth) vs Global abnormality (prediction = inactive OR boosted)

cm_overall = confusion_matrix(y_abnormal, y_global_abn, labels=[0,1], normalize=norm_mode)

results["overall_abnormal_vs_global"] = cm_overall

results["overall_abnormal_vs_global_df"] = _cm_df(cm_overall)

return results

# Example usage:

cm_results = evaluate_confusions(panel_df, normalize=False)

print("Inactive (truth) vs Abnormal (model):\n", cm_results["inactive_vs_abnormal_df"], "\n")

print("Boosted (truth) vs Abnormal (model):\n", cm_results["boosted_vs_abnormal_df"], "\n")

print("Overall: Abnormal (truth) vs Global (inactive OR boosted) prediction:\n", cm_results["overall_abnormal_vs_global_df"])

Inactive (truth) vs Abnormal (model):

Pred 0 Pred 1

True 0 3830 74

True 1 56 540

Boosted (truth) vs Abnormal (model):

Pred 0 Pred 1

True 0 3867 609

True 1 19 5

Overall: Abnormal (truth) vs Global (inactive OR boosted) prediction:

Pred 0 Pred 1

True 0 3811 75

True 1 69 545